Who is really setting the pace in Bitcoin demand now: the ETF complex, or Michael Saylor’s corporate treasury machine? As ETF flows cool and market sentiment stays fragile, Joe Consorti argues that Strategy has done something more important than merely buy more BTC than BlackRock’s IBIT, it has shown it can keep accumulating aggressively even in a weak tape.

The core thesis: Strategy’s funding engine is still working when bears expected it to fail

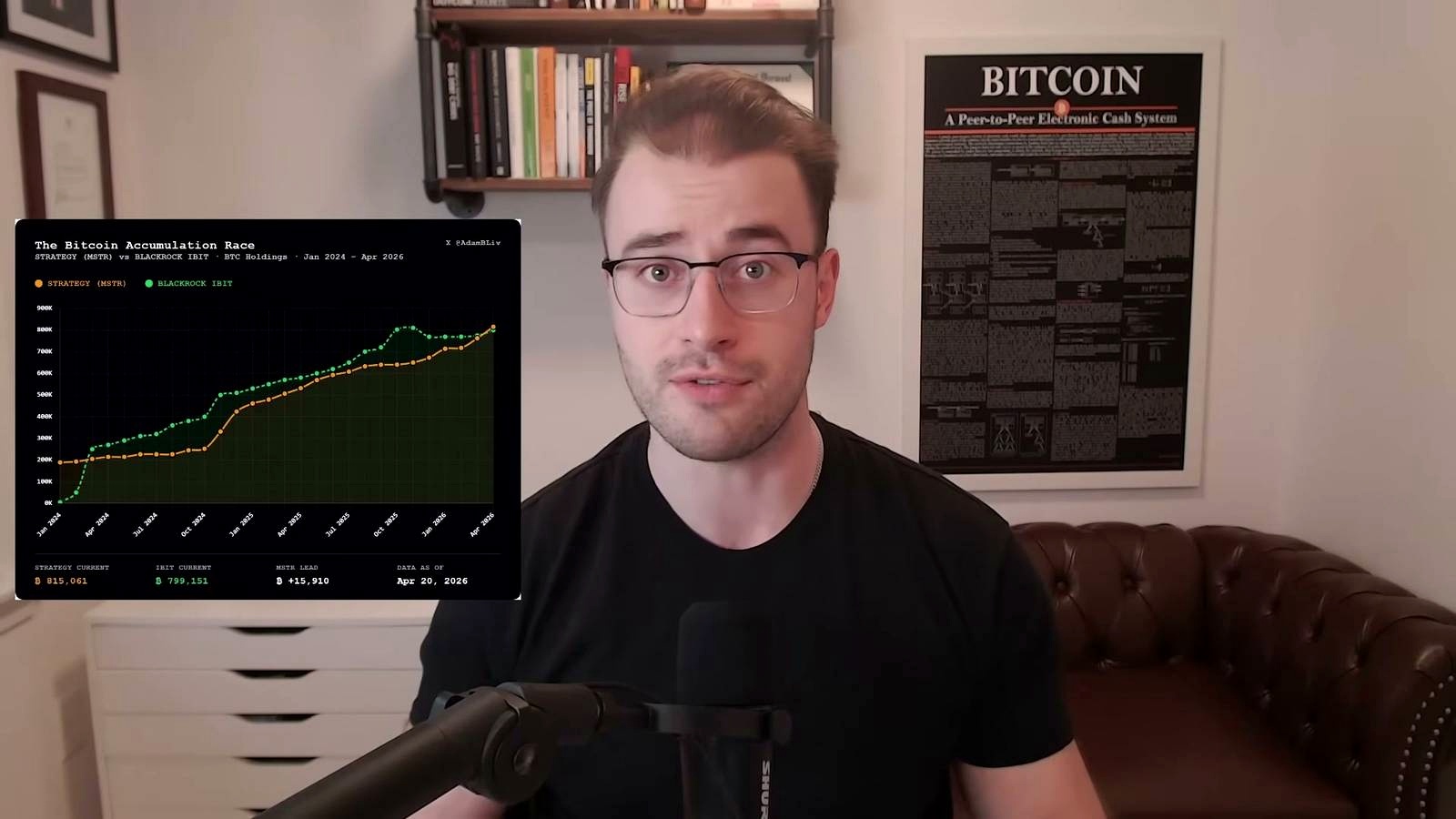

According to Joe Consorti, the key development is not simply that Strategy now holds roughly 815,061 BTC, ahead of BlackRock’s iShares Bitcoin Trust at about 803,000 BTC, after adding 34,164 BTC in a single week. It is that the company did so while Bitcoin was still down more than 40% from its prior all-time high, in what he described as the worst sentiment backdrop since 2022.

That matters because one of the longest-running bear cases against Strategy has been straightforward: the model only works in a rising market. If Bitcoin falls, the stock premium compresses, capital raising gets harder, and the flywheel slows. Consorti’s argument is that last week was the clearest counterexample yet. Strategy’s purchase, worth about $2.54 billion at an average price of $74,395, was, in his telling, the third-largest weekly acquisition in company history and the largest ever made in a bear-market regime.

The broader market context makes that claim notable. Spot Bitcoin ETFs remain a major structural source of demand, but they are ultimately pass-through vehicles whose holdings depend on net investor inflows. Corporate treasury buying is different: it can be more discretionary, more leveraged to market structure, and more reflexive. In periods when ETF flows flatten, a single large buyer can still matter if it has reliable access to capital.

That said, Consorti’s framing is more bullish than consensus. Many investors still see Strategy less as a simple Bitcoin proxy and more as a highly levered, premium-sensitive vehicle whose access to capital depends on investor appetite for Saylor’s structure. Bulls view that as a feature. Critics view it as a cycle-dependent vulnerability.

How the latest BTC buy was funded, and why Consorti says that changes the story

According to Joe Consorti, about 86.8% of the latest purchase, or roughly $2.18 billion of the $2.54 billion total, came from a preferred equity instrument he calls Strategy’s “variable rate series A perpetual stretch preferred stock.” He argues this is the underappreciated mechanism allowing the company to keep converting capital-market demand into spot Bitcoin purchases.

He said Strategy sold 21.8 million shares of that preferred and generated $2.18 billion in gross proceeds. He also pointed to an ATM capture rate of about 80% last week, versus 79% the week before, his way of measuring how much trading demand in the instrument is effectively captured by Strategy and turned into Bitcoin buying.

Consorti further argued that the preferred’s stated yield of 11.5% compares favorably with the roughly 5.4% available in U.S. investment-grade corporate bonds and around 7.8% in high-yield debt. In his view, that creates a structural bid from fixed-income buyers that can continue even when Bitcoin itself is weak.

His supply-side framing is aggressive. Strategy’s weekly buy of 34,164 BTC compares with current post-halving issuance of just 450 BTC per day, or around 13,500 BTC per month. By that math, the company absorbed nearly 11 weeks of new supply in 7 days. He also cited two trading sessions, April 13 and April 14, that implied purchasing power equal to 7,741 BTC and 9,500 BTC, respectively.

The larger point is that Consorti sees this as a throughput story, not a one-off buy. Before this preferred-stock channel, he said Strategy’s major purchase cadence was roughly every 3 to 6 weeks. With an 80% capture rate and a proposal to move dividends from monthly to semi-monthly, he argues the company could announce purchases every two weeks if the instrument continues trading at or above par.

That is where his thesis becomes most consequential for Bitcoin markets. If a single public company can repeatedly absorb supply faster than miners create it, it changes the short-term float picture. Traders have seen versions of this before with ETF inflows: when a structural buyer keeps returning, price can become more sensitive to any reduction in available sell-side liquidity.

What could go wrong with this thesis

Consorti says the scenario that breaks the model is not another 20% decline in Bitcoin, but Bitcoin going to zero. That is a strong claim, and probably too strong.

The more realistic challenge is not literal collapse, but deterioration in the conditions that make Strategy’s capital-raising machine function. If the preferred stock stops trading at or above par, the ATM economics weaken. If demand for the instrument fades, throughput falls. If Strategy’s equity valuation compresses hard enough, investor appetite for related securities could cool across the capital stack. In that scenario, the company may still buy Bitcoin, but at a slower pace and on less attractive terms.

There are other risks the bullish framing underplays. One is refinancing and liability management risk across Strategy’s broader balance sheet. Another is market crowding: if too much of the bull case for both MSTR and BTC starts depending on continued issuance into strong demand, any disruption can produce reflexive downside. There is also regulatory and governance risk around how far public-market investors are willing to support an increasingly financialized Bitcoin accumulation vehicle.

The other side of the trade is clear. ETF buyers get cleaner exposure to spot BTC, generally with lower complexity and lower company-specific risk. Strategy holders are buying an active, levered accumulator. That can outperform in favorable conditions, but it also introduces execution, funding, and valuation risk that an ETF largely avoids.

What to watch next

The most immediate trigger is whether Strategy keeps buying on the accelerated cadence Consorti outlined. If new purchases start appearing every two weeks, the market will take the preferred-stock funding channel more seriously.

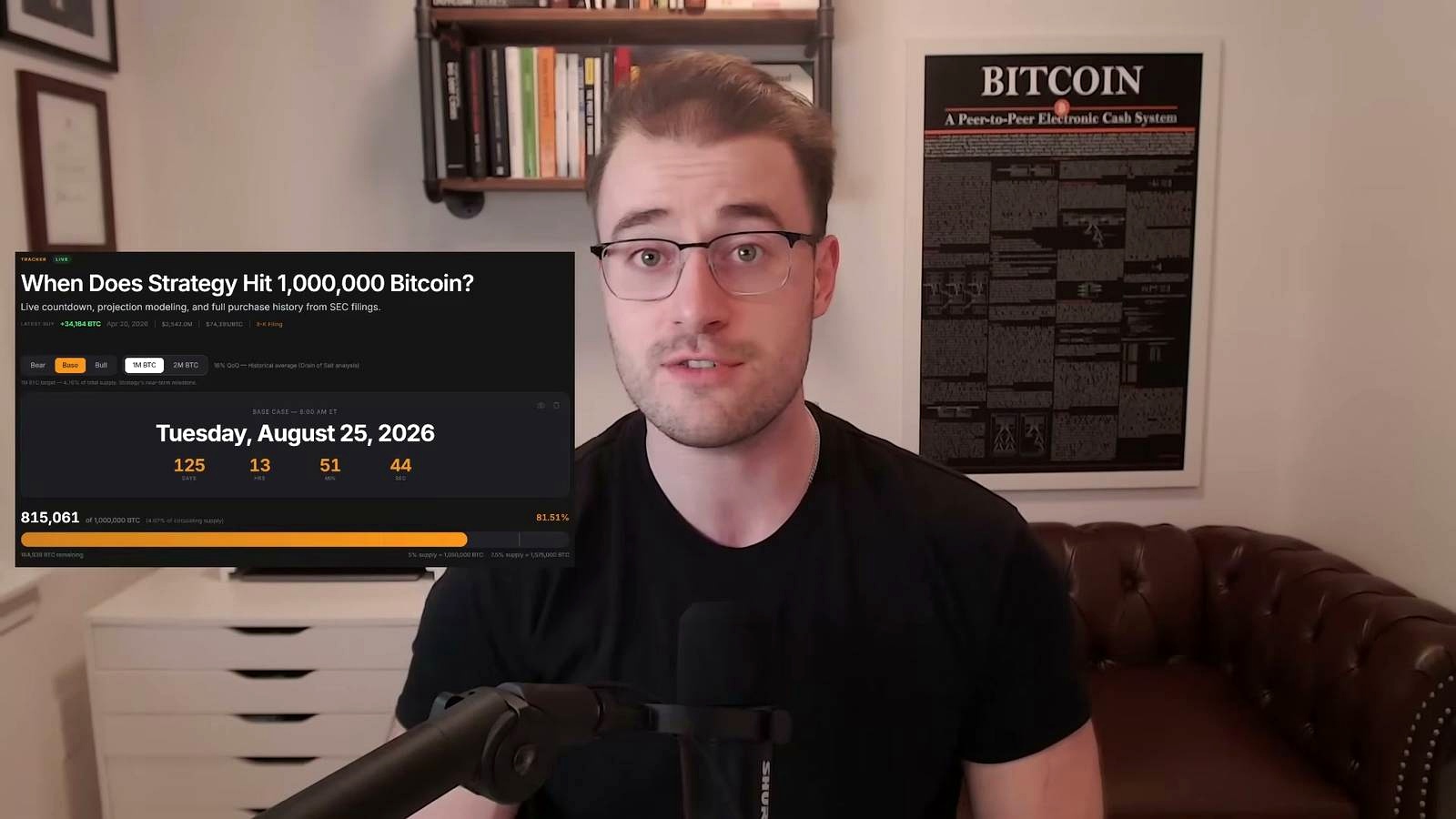

Investors should also watch whether the preferred continues to trade at or above par, since that is central to the ATM capture mechanism. On the Bitcoin side, the headline milestone is Strategy’s path to 1 million BTC. Consorti’s base case places that at August 25, 2026, or about 125 days from the video’s timeline, requiring another 184,939 BTC.

Further out, the next halving in April 2028 would cut daily issuance from 450 BTC to 225 BTC. If Strategy is still buying at anything close to the current pace by then, supply absorption becomes a much bigger market issue.

FAQ

What does “trading at or above par” mean for a preferred stock?

Par is the security’s reference face value, often the level around which issuance economics are built. If a preferred trades at or above par, the issuer can usually sell more of it on better terms. If it trades below par, raising fresh capital becomes less efficient or unattractive.

How is Strategy different from a spot Bitcoin ETF like IBIT?

A spot ETF is designed to track Bitcoin and pass through price exposure, minus fees. Strategy is an operating company that actively raises capital and uses it to buy more Bitcoin. That means it can increase Bitcoin per share over time, but it also carries corporate, financing, and execution risks that an ETF does not.

What is Bitcoin “yield” in the context of Strategy?

In this context, it does not mean staking or on-chain yield. It refers to growth in Bitcoin holdings on a per-share basis. Consorti cited Strategy’s year-to-date Bitcoin yield at 9.5%, meaning existing shareholders effectively gained exposure to more BTC per share over that period.

Why does miner issuance matter for Bitcoin’s price?

Miner issuance is the new supply entering the market each day. After the halving, that flow dropped to about 450 BTC per day. When a large buyer absorbs more than that on a sustained basis, it can tighten available supply and make price more responsive to incremental demand.

What happened the last time a single buyer dominated Bitcoin demand?

The closest parallel is the launch phase of U.S. spot ETFs, when persistent inflows helped absorb available BTC and reshape market structure. The difference here is that ETF demand depends on investor subscriptions, while Strategy’s model depends on capital-market issuance and investor demand for the company’s securities.

Source Video

An Indian crypto journalist covering the developments in the Bitcoin and blockchain industries. Her work helps readers understand key changes in the world of digital assets.