MicroStrategy’s pitch has long been simple: if you want amplified Bitcoin exposure in public markets, buy the stock. But that trade looks less automatic when BTC rises and MSTR still lags. According to MSTR Investor, that underperformance is a warning that Strategy’s financing machine may be losing some of its short-term edge just as macro and geopolitical risks rise.

Why the MSTR-underperformance story matters now

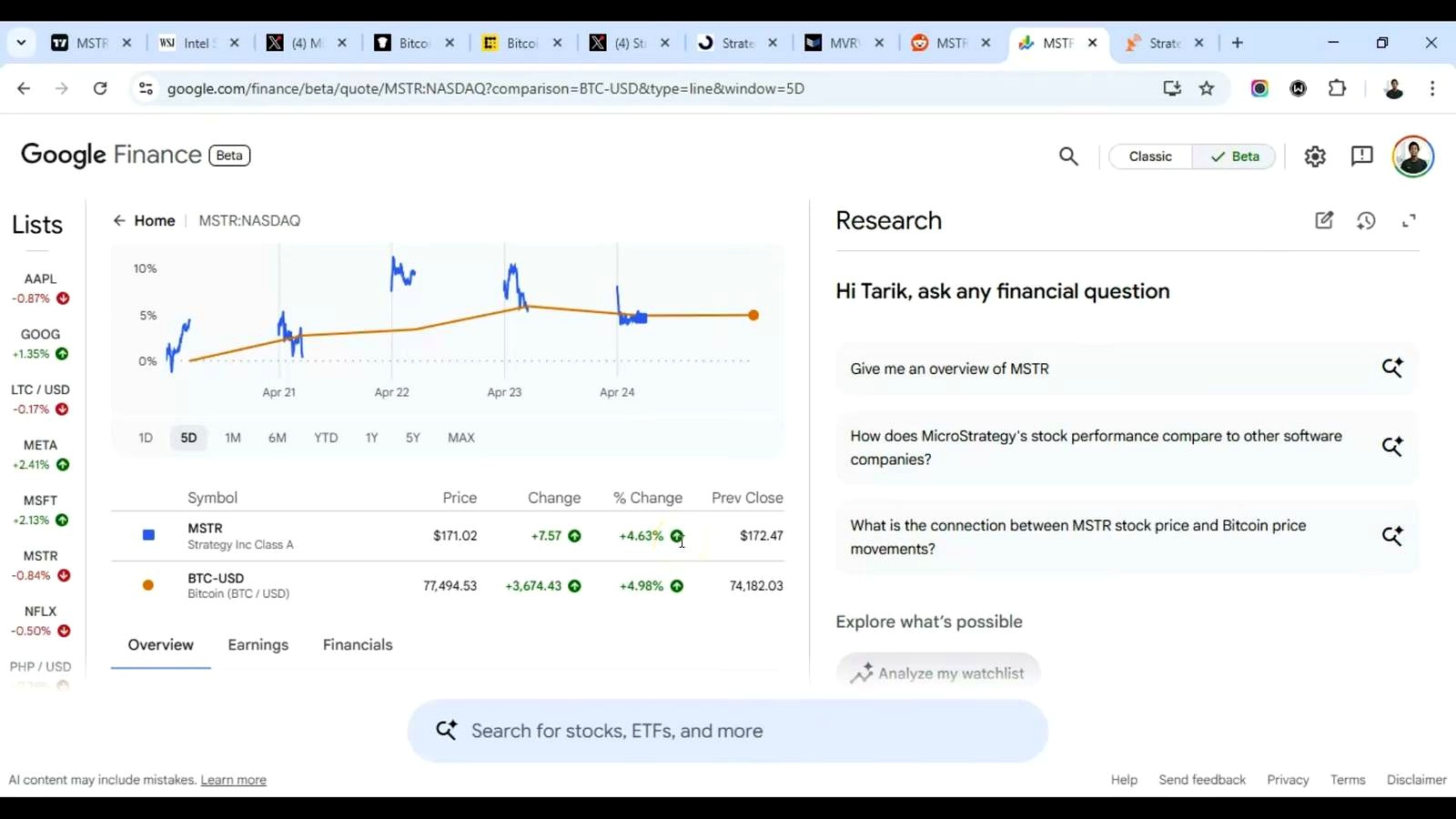

According to MSTR Investor, Bitcoin gained roughly 5.15% on the week, while Google Finance showed BTC up about 5% over the last 5 trading days and MSTR up just 4.63%. For a stock widely treated as a leveraged Bitcoin proxy, that gap is the point.

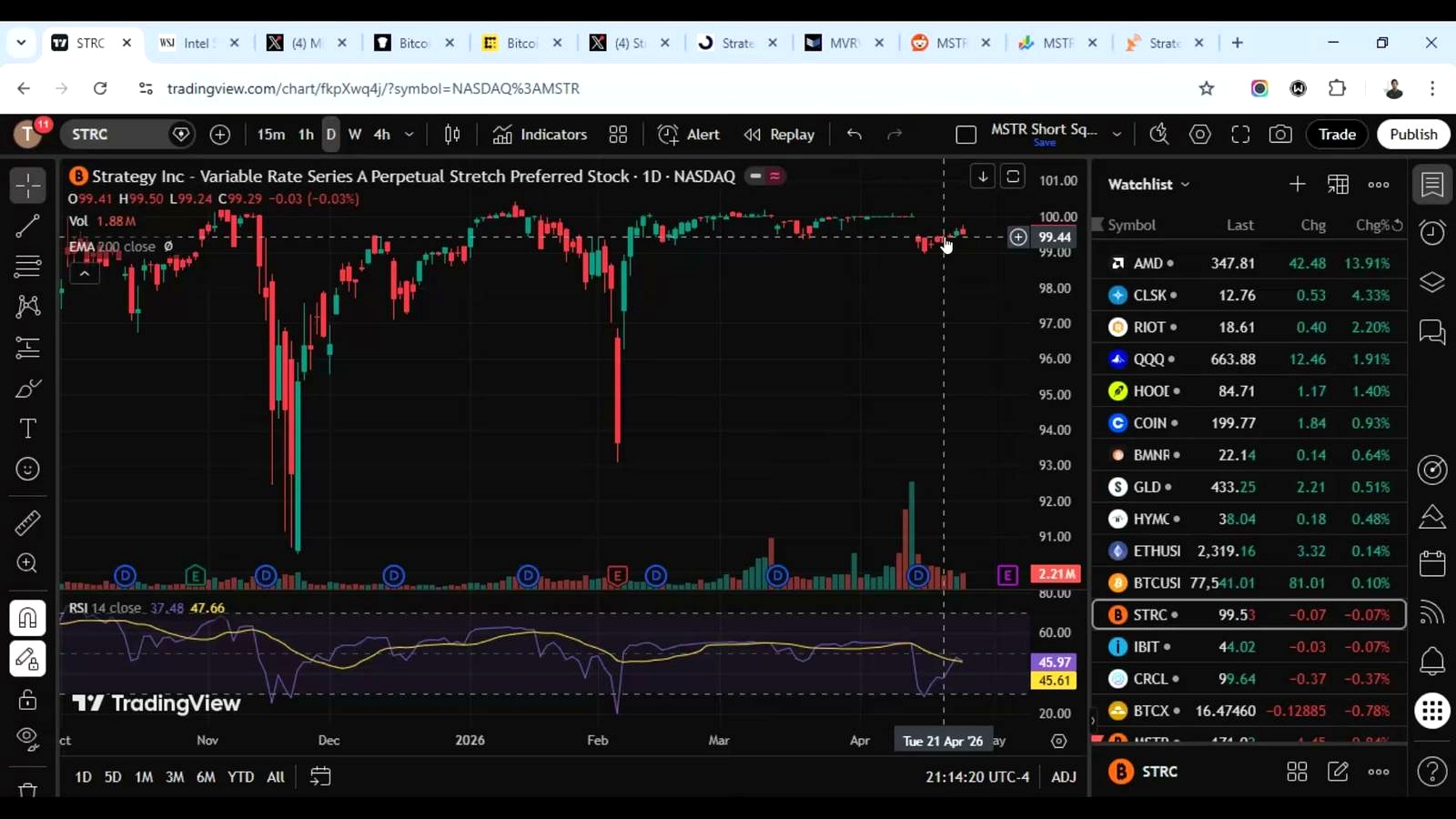

The host’s core argument is that MSTR’s weaker relative performance is not random. He argues it reflects a shift in how Strategy can fund Bitcoin purchases. In his telling, the company’s newer preferred-style capital vehicle, STRC, is highly effective when it trades above $100, but far less useful when it stays below that level. He says STRC traded under $100 for most of the week and had remained below $100 since the ex-dividend date on April 15. If that is true, the analyst argues, Strategy would be less able to use the STRC ATM and more likely to rely on the common-stock MSTR ATM instead.

That distinction matters because selling common equity directly increases share count and can pressure the stock, especially in periods when investors are already questioning premium valuation. According to MSTR Investor, that is one reason MSTR failed to break above $180 and underperformed Bitcoin this week.

In broader market context, this is a more cautious view than the bullish consensus that often surrounds Strategy during strong BTC stretches. Many MSTR bulls argue the stock should outperform over time because it combines Bitcoin treasury exposure with capital markets optionality. The bearish counter is that this optionality cuts both ways: if preferred issuance loses efficiency or the equity premium compresses, MSTR can briefly trade like a diluted proxy rather than a turbocharged one.

The analyst’s thesis: macro rotation, financing friction, and an overbought chart

According to MSTR Investor, there are three forces hitting MSTR at once.

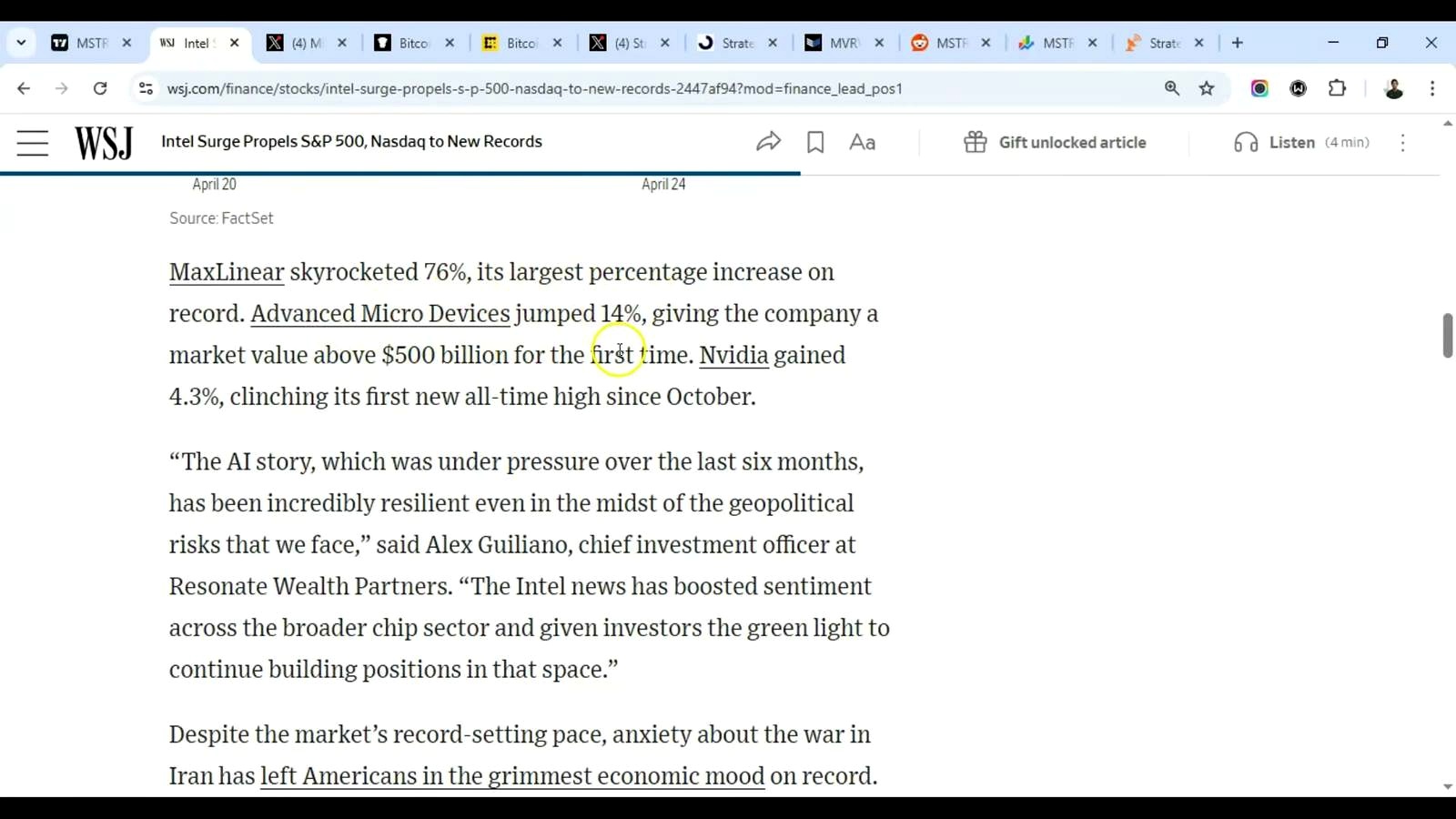

First, he sees capital rotating elsewhere. He points to a strong AI-chip trade, citing Intel up 24%, AMD up 14%, and MaxLinear up 76%. He also notes the Nasdaq rose 1.6% to its fifth all-time high of the year, while the S&P 500 added 0.8% for its ninth record of 2026. His read is that investors are looking past geopolitical tension and chasing semiconductor momentum instead of piling into Bitcoin-linked equities.

Second, he ties crypto softness to macro stress. He references Brent crude above $105, U.S. crude at $94, and Japanese inflation data showing the corporate service price index rising 3.1% year-on-year in March versus a 3.0% forecast. He also mentions a hawkish Bank of Japan and war-related jitters tied to Iran. The broader implication is that liquidity-sensitive trades can struggle when inflation and energy shocks return to the foreground.

Third, he argues MSTR itself is stretched. The analyst says the stock’s daily RSI has reached an overbought region not seen since July 2025, with similar prior episodes in May 2025 and December 2024 followed by sell-offs. In his framework, that technical backdrop combines with issuance-related pressure to create a setup where MSTR can lag BTC even if Bitcoin remains relatively stable.

This is a notably contrarian stance in a market that often buys MSTR on any sign of BTC strength. It also leans heavily on technical and structural reasoning rather than a fundamental challenge to Bitcoin itself.

Secondary signals: STRC growth, resistance at $177, and the trade setup

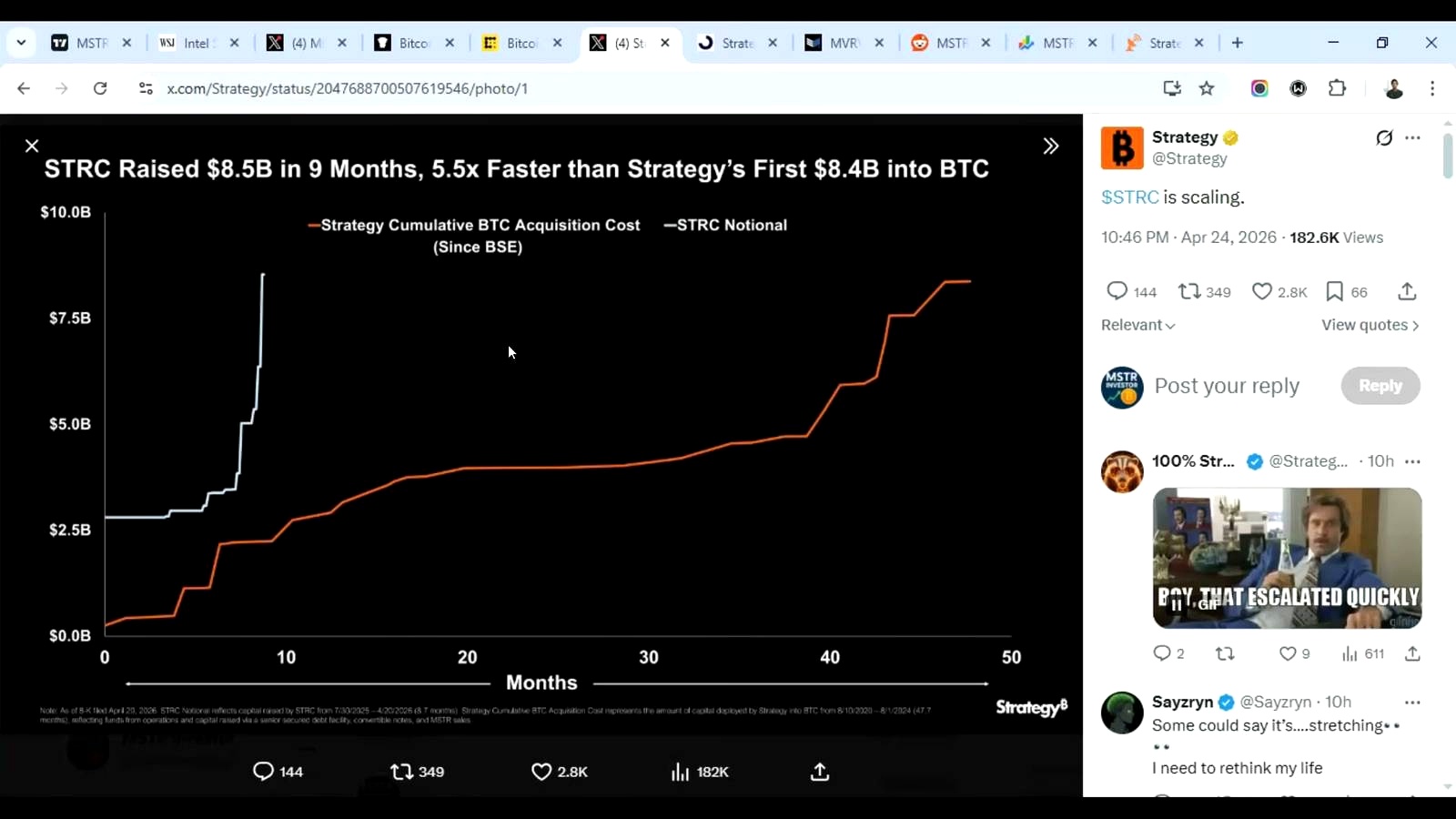

The analyst is not arguing that Strategy’s newer financing tools have failed outright. In fact, he says STRC has scaled quickly. He cites company messaging that STRC raised $8.5 billion in 9 months, compared with Strategy’s first $8.4 billion into Bitcoin at a pace he says was 5.5 times slower. He also points to STRC’s advertised yield of 11.5%, contrasting that with typical high-yield savings returns of less than 4%.

That is an important nuance. According to MSTR Investor, STRC is attractive precisely because it can bring in capital without leaning as hard on common-share dilution. But he says the mechanism is price-sensitive: below $100, the product loses practical usefulness as a Bitcoin acquisition engine. In his telling, that leaves Strategy back at its “old bread and butter” of issuing common equity, which can cap upside for existing shareholders.

On the chart, the host highlights the 200-week exponential moving average near $177 as a major resistance zone. He says MSTR has been rejected there for 2 weeks in a row. He also dismisses the idea that a clean move to $200 is imminent, arguing instead for a retest of roughly $130 to $140. Later in the video, he says he expects MSTR to be around $130 to $150 by the end of June.

His practical trade expression follows from that view. He says he would continue selling covered calls, rolling them into May and June, which he describes as historically weaker months. For longer-dated bullish exposure, he says he plans to buy December 2028 LEAPS at the end of Q2, aiming to position for a move roughly 250 days after the 2028 halving in July.

What could go wrong with this thesis

The cleanest way this bearish MSTR call fails is if Bitcoin simply breaks higher and pulls Strategy’s equity premium back with it. MSTR has repeatedly shown that when BTC momentum turns forceful enough, concerns about dilution or financing mechanics can get overwhelmed by demand for levered exposure. A sharp move in Bitcoin could make a $177 resistance break look more important than this week’s underperformance.

There is also a structural counterargument the analyst only partly addresses. Even if STRC trades below $100 temporarily, Strategy still has multiple ways to raise capital, and markets may continue rewarding the company for expanding its Bitcoin stack over time. Investors who own MSTR are often explicitly accepting dilution risk in exchange for treasury growth and volatility capture. That investor base may prove more tolerant than bears expect.

The on-chain argument also has limits. According to MSTR Investor, the Bitcoin MVRV Z-score has historically bottomed in a “blue box, ” and because the current cycle has not fully entered that region, he believes the bear market is not over. But historical analogs are not rules. Bitcoin’s market structure has changed over time, with institutional participation, ETF-related flows, and broader derivatives depth potentially altering how cycle bottoms form.

Finally, his macro framing can cut both ways. Geopolitical shocks and inflation scares can pressure risk assets, but they can also revive the long-term hard-asset case for Bitcoin if fiat credibility or sovereign risk becomes the bigger market story.

What to watch next

The immediate trigger is whether MSTR can reclaim and hold above the $177 area, which the analyst ties to the 200-week EMA. A clean move through that zone would weaken the near-term bearish setup.

Investors also need to watch whether STRC gets back above $100. In the host’s framework, that would improve Strategy’s ability to fund Bitcoin purchases without relying as heavily on common-share issuance.

On the macro side, oil remains a live variable with Brent above $105, and the ceasefire timeline he mentions runs through May 21. For Bitcoin specifically, the analyst is watching for a deeper move in the MVRV Z-score toward the historical “blue box” bottoming region. If that never materializes and BTC strengthens anyway, his call for MSTR to retest $130 to $140 becomes much harder to defend.

FAQ

What is the Bitcoin MVRV Z-score?

The MVRV Z-score is an on-chain valuation metric that compares Bitcoin’s market value with realized value, or the aggregate price at which coins last moved. Traders use it to gauge when BTC may be historically overvalued or undervalued.

Why can MSTR underperform Bitcoin if it is supposed to be leveraged BTC exposure?

MSTR is a stock, not a futures contract. Its performance depends not just on Bitcoin, but also on equity market sentiment, valuation premium, dilution from capital raises, options flows, and company-specific financing mechanics.

What does it mean when STRC trades below par?

Below par means below its reference value of $100. In the analyst’s framework, that matters because he believes Strategy is less likely to use STRC as an ATM funding source for additional Bitcoin purchases when it trades under that level.

What are LEAPS, and why would someone use them for MSTR?

LEAPS are long-dated options, often expiring more than a year out. Traders use them to express a bullish or bearish view with less upfront capital than buying shares, though they add time decay and volatility risk.

What happened the last times MSTR reached overbought daily RSI levels?

According to MSTR Investor, similar daily RSI readings appeared around December 2024, May 2025, and July 2025, and each was followed by a sell-off. Traders treat RSI as a momentum gauge, not a standalone timing tool.

Video Reference

An Indian crypto journalist covering the developments in the Bitcoin and blockchain industries. Her work helps readers understand key changes in the world of digital assets.