Small-scale Bitcoin miners are chasing a familiar problem: how to keep the lottery-like upside of solo mining without absorbing all of the downside. Parasite Pool’s second block, found roughly 2 months after its first and then followed by another hit just 6 days before Sterling’s video, has put that question back on the table.

The Core Thesis

According to Sterling, Parasite Pool’s latest block strengthens the case for a hybrid mining model that blends solo-mining upside with partial pooled payouts. The structure he describes is simple but unusual: 1 Bitcoin from the block goes to the miner who actually finds it, while the remaining 2.125 BTC is distributed among pool participants based on proportional work contributed to that block.

Sterling argues the second block produced a better effective payout than the first because it was found much faster. In his framing, that matters because Parasite Pool uses a proportional-share model, meaning returns depend not just on how much work miners submit, but also on how quickly a block is found. He says the pool’s first block came after roughly a year of operation, while the latest was found on April 18 and arrived far sooner after the previous hit, boosting payouts for those who had contributed work during that shorter interval.

This is a niche but increasingly relevant debate in Bitcoin mining. Post-halving, margins are tighter, transaction fees are more volatile, and smaller miners are under pressure from industrial-scale competition. In that environment, alternative pool structures can attract attention even if they do not change the underlying math of mining. The broader market consensus still favors traditional pooled mining for stable cash flow and conventional solo mining for pure jackpot exposure. Parasite Pool’s model sits somewhere between those poles.

The attraction is obvious: for hobbyist or low-hash miners, the pool offers some cost recovery without fully giving up the possibility of landing a 1 BTC winner-take-most outcome. But the counterweight is just as important. Over time, expected returns in mining tend to compress toward network averages after fees, variance, and electricity costs. Sterling acknowledges as much, saying the early-stage profitability should decline as more hash rate joins.

Why the Second Block Matters

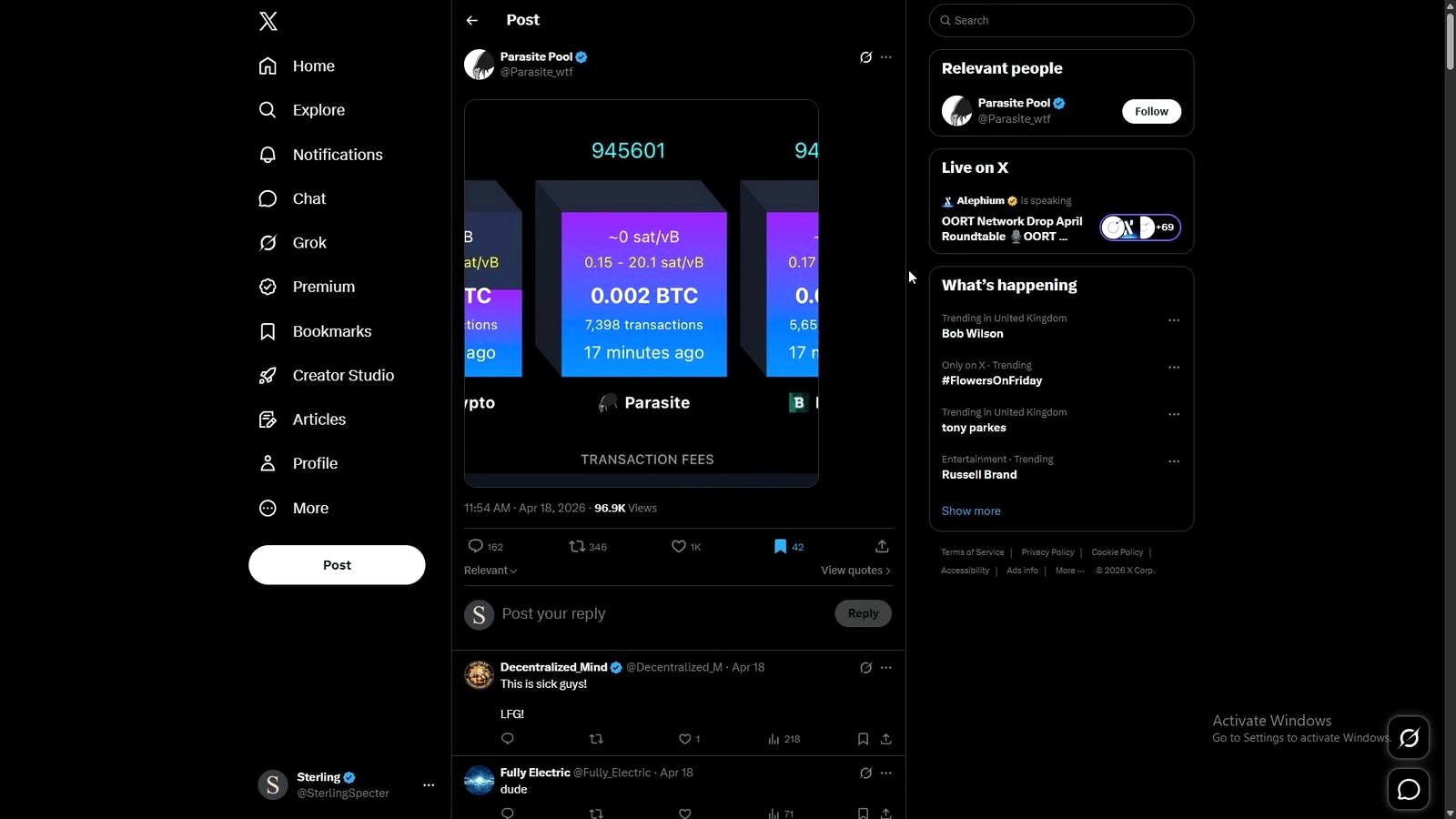

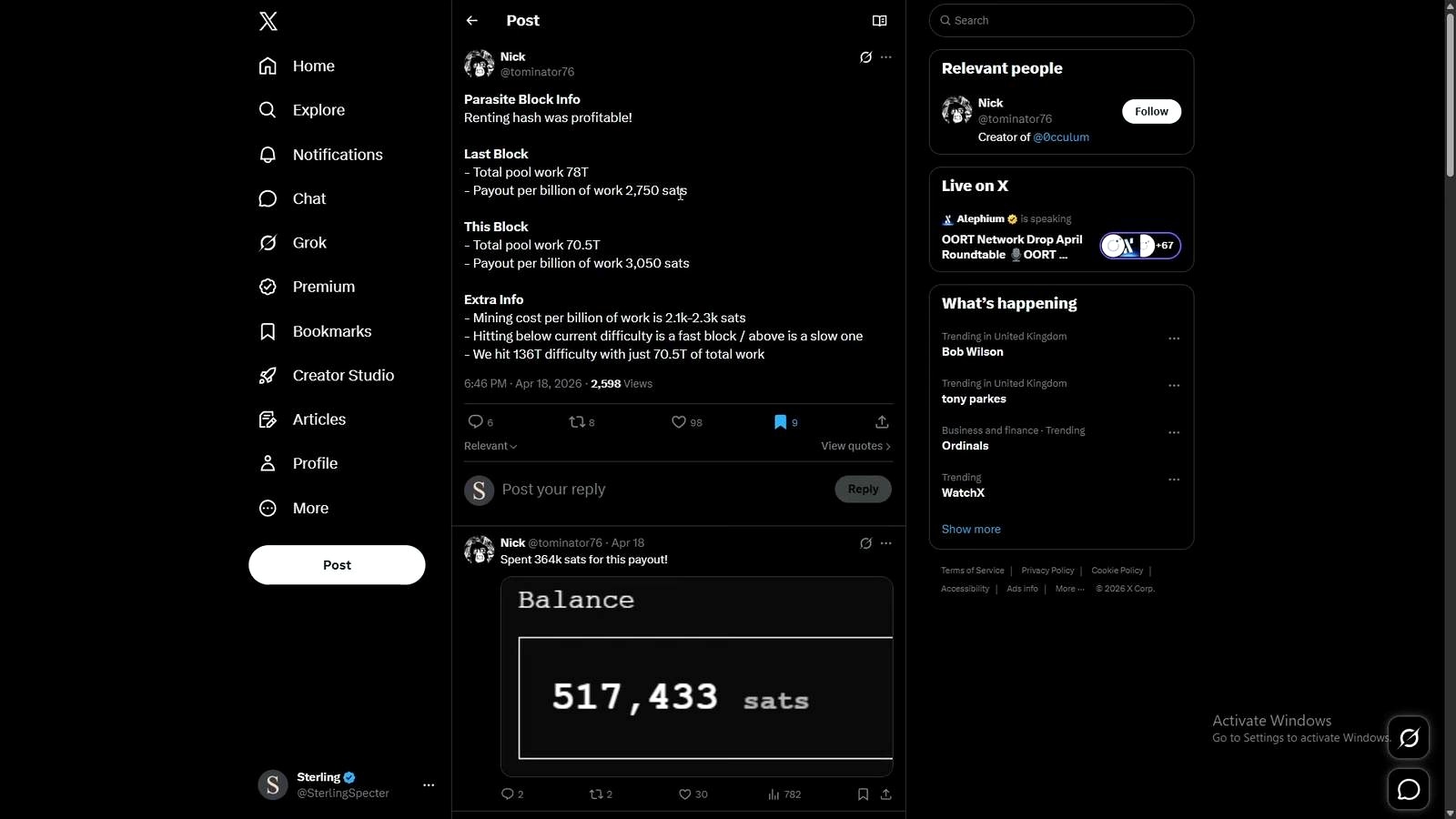

According to Sterling, the biggest data point from the second block was not merely that it happened, but how the pool’s internal economics changed. He cites total work on the first block at 78 trillion, with a payout of 2,750 sats per billion of work. For the second block, he says total work was about 8 trillion lower, implying roughly 70 trillion of work, which pushed payout per unit of work higher.

That fits the model he describes. If fewer cumulative shares are submitted before a winning block arrives, each unit of contributed work captures a larger portion of the 2.125 BTC shared payout. Sterling also points to anecdotal profitability for rented hash power, citing mining costs of 1.2 to 2.3 per billion of work and a reported profit of around 900 sats per billion of work for at least one participant. He also mentions another participant spending 364k, apparently in sats, while discussing hash-rental economics.

That is where the story gets more complicated. Short bursts of rented hash rate can distort a proportional pool. Sterling says users can “blast” large amounts of hash power onto the network for a few hours, accumulate a meaningful share of work, and then benefit later if the pool finds a block. He points to a spike to around 2.85 exahash and suggests that level was likely rented rather than organic miner growth.

This matters because it cuts both ways. On one hand, rented hash can accelerate block discovery and make the pool feel more active. On the other, it can dilute smaller continuous miners who are contributing with home rigs rather than tactical bursts of rented capacity. For Bitcoin miners evaluating the pool, the key question is not just whether the pool can find blocks, but who captures the economics when it does.

Sterling also highlights rising participation. He says users were around 800 when he had been mining there earlier, and that both users and workers had climbed since about March 26. He interprets much of that increase as likely tied to rented hash activity, not necessarily a broad wave of retail hobbyists plugging in new machines.

What Could Go Wrong

The clearest challenge to Sterling’s constructive view is that early outperformance may be little more than variance. Fast blocks make any proportional system look attractive in hindsight, but a few slow rounds can reverse that impression quickly. If Parasite Pool enters a streak where it does not find a block for materially longer than expected, miners may discover that the “recoup some costs” pitch still leaves them underperforming standard pools with steadier payouts.

Another risk is adverse selection from hash renters. If sophisticated participants only appear when rental markets make short-term attacks on the payout structure economical, smaller miners could end up subsidizing opportunistic behavior. Sterling notes that this has already become a feature of the pool’s activity. He presents that as part of the current reality, but not necessarily as a solved design problem.

There is also a structural issue he mentions but does not fully unpack: Bitcoin mining itself “isn’t really profitable” in many setups, even when block rewards are available. That is especially true for miners with high residential power costs, older ASICs, or poor uptime. A hybrid pool does not eliminate those constraints. It mainly changes how variance is distributed.

Finally, there is a community-layer risk. Sterling ties some of the pool’s momentum to the Ordinal Maxi Biz ecosystem and to hardware tied to that community. If interest in that subculture cools, some of the growth in users, rented hash, and attention could fade with it. A mining pool built around novelty still has to survive the dull arithmetic of long-run expected value.

What to Watch Next

The next real signal is whether Parasite Pool can sustain its growth in hash rate without depending on short-lived rental spikes. Sterling says the pool had been projecting around a 60-day average time to find a block in a prior look, but that activity has changed materially since then.

Watch three things: whether average hash rate stays elevated after burst activity fades, whether another block arrives on a timetable consistent with that stronger participation, and whether payout per unit of work remains attractive as more miners join. Sterling’s own forecast is that the pool could hit 4 or 5 blocks by year-end if hash rate keeps increasing. If block cadence slows sharply or rented hash dominates contribution, that thesis gets weaker fast.

FAQ

What is proportional-share mining?

Proportional-share mining distributes rewards based on how much work, usually measured in shares, each participant contributes during a round. If a block is found quickly, each submitted share can end up being worth more than in a long round.

How is this different from normal solo mining?

In normal solo mining, the miner who finds the block keeps the full reward and everyone else gets nothing. In the Parasite Pool structure described by Sterling, the block finder gets 1 BTC, while 2.125 BTC is shared across participants based on contributed work.

Why would miners rent hash rate instead of using their own machines?

Hash rental lets miners temporarily access large amounts of computing power without owning hardware. Traders use it to target short-term opportunities, especially when they think a pool’s payout structure or current block luck creates a favorable setup.

What does a spike to 2.85 exahash suggest?

A move to around 2.85 exahash on a niche pool is large enough to raise questions about whether the increase came from permanent miners or temporary rented hash. Sterling believes that spike was probably rented capacity.

What happened last time Parasite Pool found a block?

According to Sterling, the first block came after roughly a year of pool uptime, and his own mining setup had contributed for about 6 months on and off before that hit. He says his payout from that round was over 111,000 to 113,000 sats, which he estimated at roughly $100 at the time.

Reference Video

John Burnell focuses on Bitcoin infrastructure, wallet security and blockchain technology. He writes educational articles explaining how Bitcoin works and how the technology evolves.