Risk assets are trying to push higher just as geopolitics and oil threaten to tighten financial conditions again. In that setup, the key question for Bitcoin-linked equities is whether momentum can survive a macro wobble. According to MSTR Investor, Strategy’s latest buy and a sharp rise in Bitcoin yield give MicroStrategy’s stock fresh near-term upside even as a seasonal pullback may be looming.

The Core Thesis

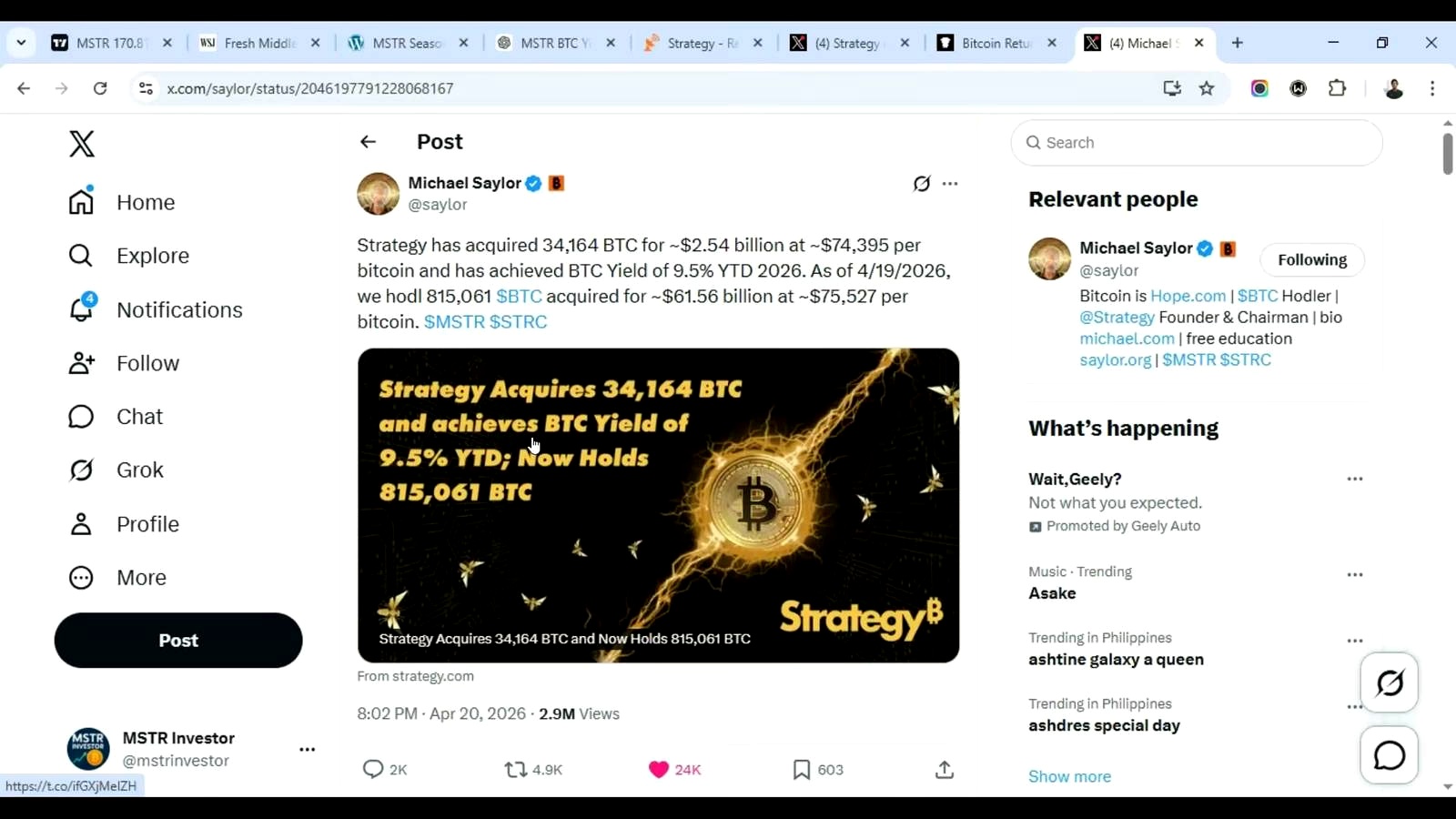

According to MSTR Investor, the central bull case is straightforward: Strategy’s latest purchase was large enough to materially improve the company’s Bitcoin-per-share economics, and that could keep supporting MSTR in the short term. The host highlighted that Strategy acquired 34,164 BTC for $2.4 billion at an average purchase price of $74,395 per coin, lifting total holdings to 815,061 BTC as of April 19, 2026. Those holdings were acquired for roughly $61.56 billion at an average price of $75,527 per Bitcoin.

He framed the purchase as Strategy’s third-largest ever and emphasized the company’s reported Bitcoin yield of 9.55% year to date, up from a start to the year when he said yield looked likely to be flat or negative. He also said Bitcoin per share had risen to 213,597, presenting that increase as the main differentiator between owning MSTR and owning spot Bitcoin or a Bitcoin ETF.

That argument sits in a familiar place in the market. Bulls have long treated MSTR as a leveraged Bitcoin vehicle with an added financial-engineering layer: if management can issue securities at favorable terms and buy BTC accretively, shareholders get rising Bitcoin exposure per share. That is the appeal. The challenge is that this works best when capital markets stay open, MSTR trades at a healthy premium to its Bitcoin value, and Bitcoin itself trends up. If any of those conditions weaken, the same leverage that drives outperformance can reverse hard.

The broader market context is mixed. Bitcoin has often shown resilience during equity volatility when the move is driven by fiat debasement or liquidity expectations, but it can also trade like a high-beta risk asset during macro stress. Rising oil above $95 a barrel, if sustained, can feed inflation concerns and reduce the odds of easier monetary policy, which is not automatically bullish for speculative equities like MSTR.

Supporting Analysis

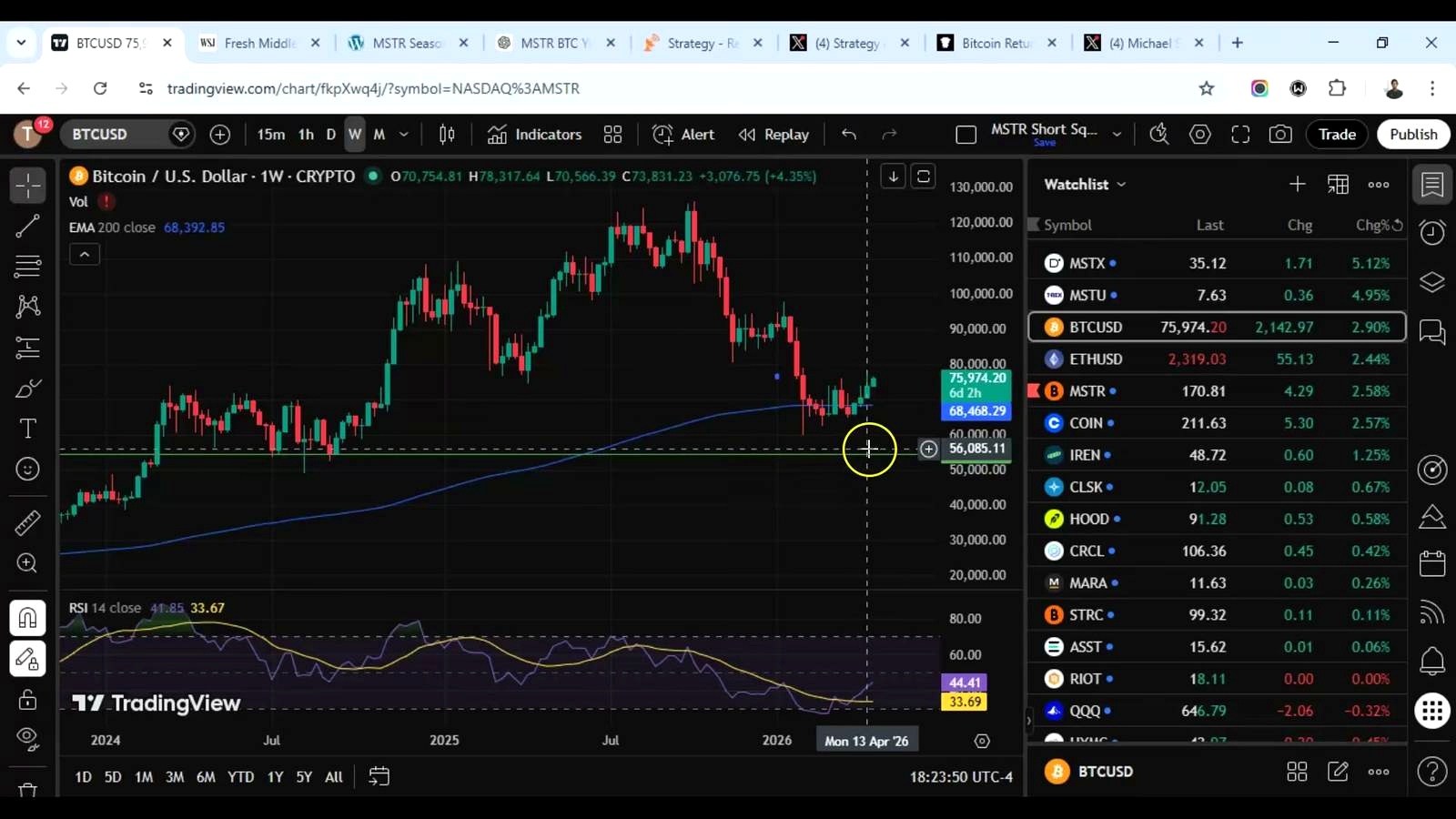

According to MSTR Investor, the near-term setup still looks constructive. He pointed to Bitcoin being on a four-week winning streak and said MSTR has now logged three straight weeks of higher highs and higher lows. He also cited recent performance numbers: MSTR rose 11% in one day last Friday, finished last week up 29%, was up another 2.58% so far this week, and had gained 36.87% in April 2026. He compared that with April 2025, when the stock was up 31%, and November 2024 as the last similarly strong month.

The analyst’s key technical level is the 200-week exponential moving average near 177, which he described as major resistance. He noted MSTR previously broke above that line during the week of December 8, 2025, reaching 198, and later touched 190 again. Based on that history, he argued MSTR could break 190 either this week or next week heading into May, with a near-term trading zone around 175 to 185 and an outside chance of approaching $200.

He also highlighted how the latest BTC purchase was financed. Roughly $2.1 billion came through STRC, which he estimated at just over 80% of the total at-the-market funding mix, while another $366 million came from MSTR common stock issuance. In his telling, that matters because the financing mix helped raise Bitcoin yield while also pushing diluted mNAV back above 1, ending about 5 months in which the shares had traded at a discount by his measure.

That financing point is important beyond the video. MSTR’s valuation has repeatedly depended on whether investors are willing to pay a premium for management’s ability to turn stock and preferred issuance into more Bitcoin exposure. When that premium expands, new issuance can be accretive to existing holders. When it contracts, dilution becomes much harder to defend.

What Could Go Wrong

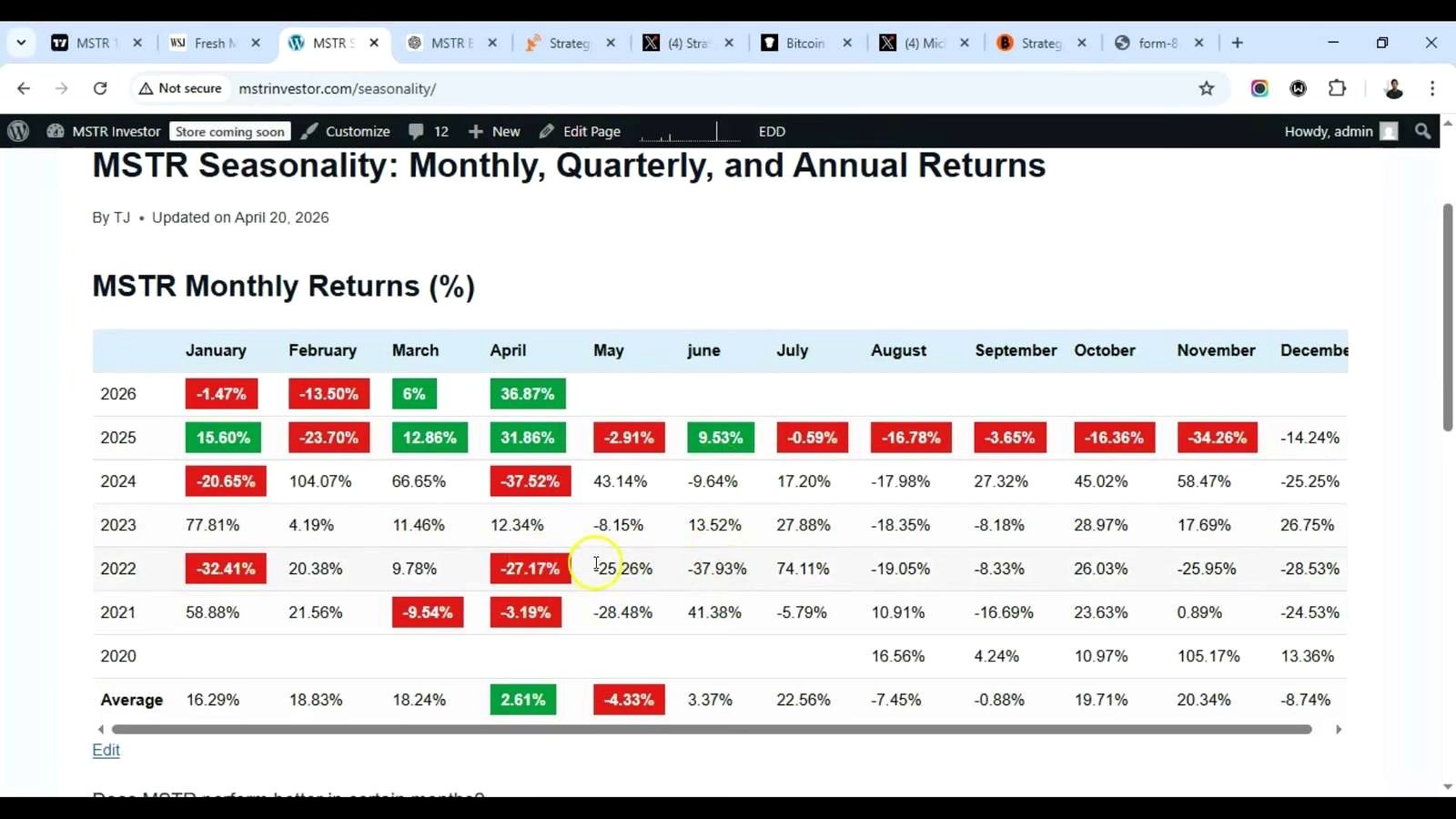

The cleanest way to break this thesis is a combination of weaker Bitcoin, tighter financing conditions, and a shrinking MSTR premium. According to MSTR Investor, the stock may have room to run for another 10 days to 2 weeks, but he is also explicitly bearish on May and June, citing “sell in May” seasonality and MSTR’s historically weak performance in those months. He said there has been only one positive May for MSTR since the company adopted the Bitcoin standard, in May 2024.

There are other risks the host touched only indirectly. Strategy financed part of this purchase by issuing more securities. That can be accretive when demand is strong, but it is still dilution. If BTC stalls near the company’s aggregate cost basis of $75,527 or falls below it, investor appetite for repeated issuance could cool quickly. A drop in Bitcoin would also pressure MSTR’s premium to net asset value, making future BTC accumulation less powerful on a per-share basis.

Then there is macro. The host noted the S&P 500 was down 0.2% while Brent crude jumped 5.6% to $95.48 amid U.S.-Iran tensions. If energy prices stay elevated, markets may begin pricing more inflation persistence and less policy easing. That tends to hit long-duration, high-volatility equities first. MSTR may be a Bitcoin story, but it still trades in the equity market and can get caught in broad de-risking.

Finally, the comparison with ETFs cuts both ways. MSTR may offer rising Bitcoin exposure per share when the model works, but spot ETFs provide cleaner BTC exposure without company-specific execution risk, capital structure complexity, or dilution.

What to Watch Next

The immediate trigger is whether MSTR can reclaim and hold above the 177 area, the host’s 200-week EMA resistance. Above that, traders will likely focus on 190 and then the $198-$200 zone he flagged from prior price action. On the downside, the key question is whether strength fades as May begins and whether “sell in May” starts showing up in both MSTR and Bitcoin.

For Strategy itself, investors should watch whether future purchases continue to improve Bitcoin yield without forcing a sharp contraction in the stock’s premium. For Bitcoin, the bigger signal is whether it can extend the current four-week run despite rising geopolitical stress and firmer oil. If BTC holds up while MSTR stays above key resistance, the bull case remains intact. If both roll over into May, the seasonal bear case gains credibility fast.

FAQ

What is Bitcoin yield in the context of Strategy?

In Strategy’s framework, Bitcoin yield refers to growth in Bitcoin exposure on a per-share basis over time. The idea is that if the company can raise capital and buy BTC accretively, each share represents more Bitcoin than before, even if an investor does not buy additional shares.

How is MSTR different from buying a spot Bitcoin ETF like IBIT?

A spot ETF is designed to track Bitcoin’s price more directly, usually minus fees. MSTR adds corporate leverage, capital markets activity, and management execution. That can lead to outperformance in bull markets, but it also introduces premium/discount dynamics and company-specific risks that ETFs do not have in the same way.

What does mNAV mean for MSTR traders?

mNAV, or multiple to net asset value, is a shorthand for how richly or cheaply MSTR trades relative to the value of its Bitcoin holdings and related assets after accounting for liabilities and dilution assumptions. When the multiple is above 1, the market is valuing the company at a premium to its underlying Bitcoin value.

Why do traders care about the 200-week EMA?

The 200-week exponential moving average is a long-term trend indicator. Traders often treat it as a major support or resistance level because it smooths out short-term volatility and highlights whether an asset is regaining or losing long-term momentum.

What does “sell in May” mean for Bitcoin-linked stocks?

“Sell in May” is a seasonal market saying based on the tendency for some equities to underperform during late spring and summer compared with the stronger part of the year. It is not a rule, but traders use it as a risk-management lens, especially for high-beta names like MSTR that have already posted large gains.

Content Source

John Burnell focuses on Bitcoin infrastructure, wallet security and blockchain technology. He writes educational articles explaining how Bitcoin works and how the technology evolves.