For a lot of people, the number sounds small. Almost dismissible. But the real story around 0.1 Bitcoin is not about fantasy wealth or overnight transformation—it’s about what happens when financial pressure starts to loosen its grip.

That’s where this conversation becomes uncomfortable, and important. Because when most households are already stretched thin, even a “small” Bitcoin position can look very different in the years ahead.

The part critics miss about 0.1 Bitcoin

The loudest criticism is simple: 0.1 Bitcoin is not enough to make someone instantly rich. That point is openly acknowledged. It is not supposed to fully retire anyone tomorrow.

The claim is narrower, but more powerful: 0.1 Bitcoin can become a meaningful financial buffer, and that buffer can change how a person lives, works, and makes decisions.

That matters more when viewed against where many people already stand financially.

The middle-class reality behind the argument

According to the Federal Reserve Survey of Consumer Finances cited in the source material, the median American has only $8,000 in transaction accounts. Half of those investing in stocks have less than $40,000.

The speaker also points to a broader reality seen over 17 years of financial coaching: 78% of people in the United States are living paycheck to paycheck with minimal savings. They worry about bills, rent, and unexpected expenses. Many are afraid of investing at all.

- Median transaction savings: $8,000

- Half of stock investors have less than: $40,000

- Share of Americans said to be living paycheck to paycheck: 78%

In that context, “not life-changing” starts to sound like a very narrow way of looking at money.

Why the number starts to matter

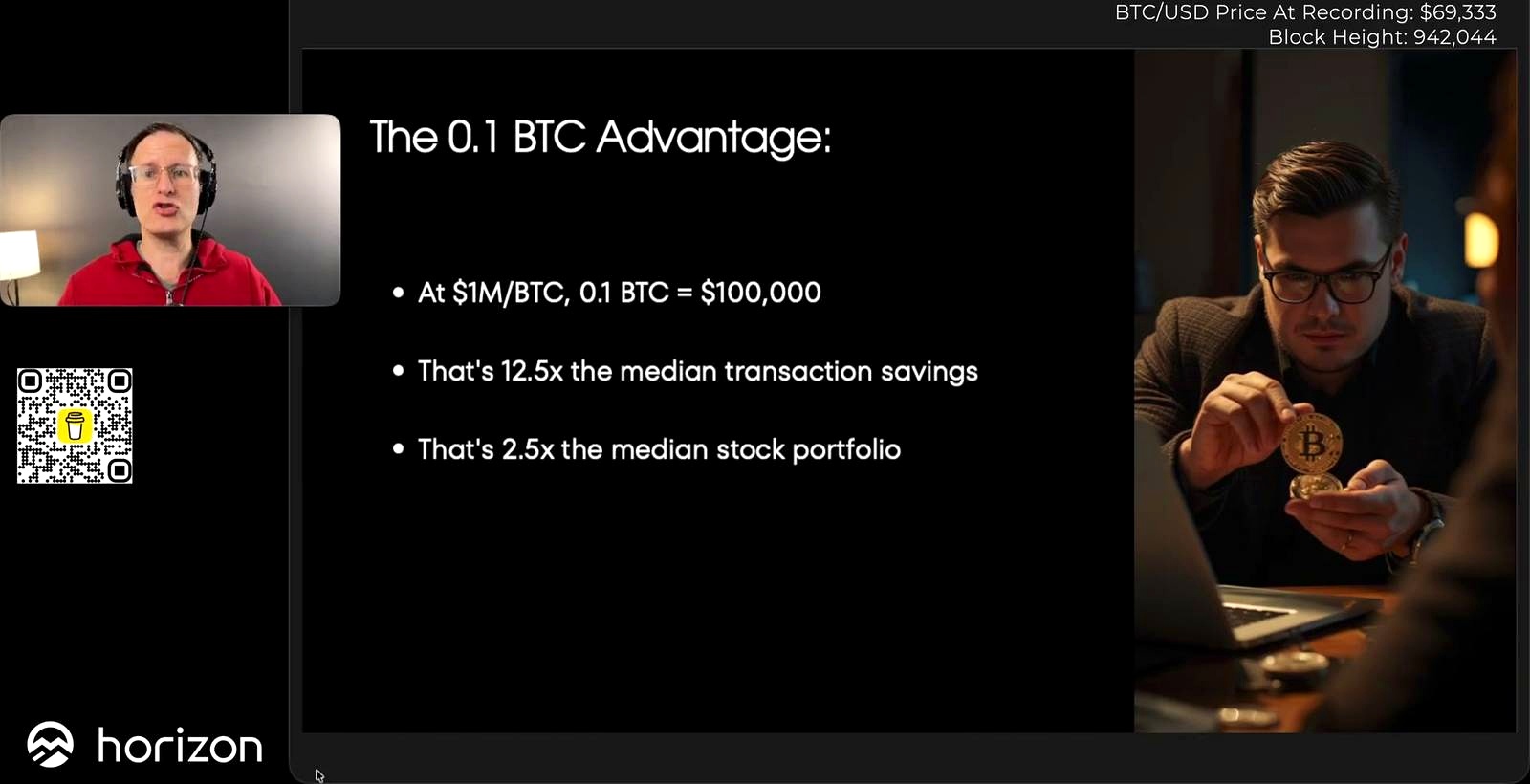

The core projection in the material is bold: within 5 to 10 years, Bitcoin could reach $1 million per coin. At that level, 0.1 Bitcoin would equal $100,000.

That figure is framed as:

- 12.5 times the median transaction savings

- 2.5 times the median stock portfolio mentioned

- Enough to cover one to two years of expenses for most people

No, that does not make someone a millionaire overnight. But for people trying to stay ahead—or just stay afloat—that kind of runway can completely alter the emotional weight of everyday life.

Stress changes everything

One of the strongest points in the material is not about price. It is about pressure.

Financial stress affects every decision. It shapes what people buy, where they work, what risks they take, and how far into the future they can even think. When savings are thin, every expense feels heavier. The example given is blunt: with $8,000 in savings, even a small purchase can feel risky.

With a larger buffer, decisions begin to shift. People can focus more on value and less on immediate price. They can think beyond the next meal, the next mortgage payment, or the next car bill.

That is why the source argues that the biggest effect of 0.1 Bitcoin may be psychological before it is anything else: less panic, more runway, more room to breathe.

The freedom angle: leaving bad situations

This is where the article’s central tension sharpens. A financial buffer does not just sit there. It changes the balance of power.

The source argues that if 0.1 Bitcoin eventually represented something like $100,000, it could give people leverage with employers and create options that do not exist when someone is trapped in survival mode.

What that leverage looks like

- Leaving a toxic employer without immediate panic

- Taking time to find work that aligns with personal values

- Making longer-term investment decisions with less fear

- Reducing money-driven pressure inside a household

The speaker ties this to personal experience: paying off $174,000 in debt changed the trajectory of life in about two and a half years. Later, being financially stronger made it possible to leave corporate America and lean fully into financial coaching.

The point is not that 0.1 Bitcoin solves every problem. It is that a real buffer can loosen the grip of bad choices made under stress.

Why 0.1 Bitcoin is also about access

Another major claim in the material is that the real value of 0.1 Bitcoin is not just the asset itself. It is access to tools that were historically out of reach for most middle-class households.

The wealthy, the source says, have long been able to borrow against assets while keeping them invested. Bitcoin, in this framing, opens that possibility more widely.

The leverage argument

If 0.1 Bitcoin were worth $100,000, the example given is that someone could potentially borrow $25,000 against it at low interest while continuing to hold the Bitcoin. That means:

- No need to sell the asset

- No taxable event from selling

- Continued exposure to long-term appreciation

This is presented as a version of the same playbook the wealthy have long used: buy, borrow, die. The difference, according to the source, is that Bitcoin democratizes that strategy for people who previously only had cash or high-interest debt available to them.

That does not mean everyone has access right now. But the article’s argument is that 0.1 Bitcoin can become the threshold where those financial tools begin to open up.

The long-term timeline changes the whole picture

The most aggressive part of the material is the long-range projection. The argument is that if Bitcoin continues appreciating, then expenses rise in fiat terms but fall in Bitcoin terms.

That is described as the key advantage of saving in an appreciating asset instead of relying only on traditional savings.

The projections in the source material

- At $1 million per Bitcoin, 0.1 Bitcoin = $100,000

- By 2029, 0.1 Bitcoin is projected in the material at $2.81 million

- By 2065, 0.1 Bitcoin is projected in the material at $5 million

The source then maps those numbers against annual fiat expenses:

- At $100,000, about 1.7 years of expenses covered

- At $2.81 million with $300,000 annual expenses, about 10 years of runway

- At $5 million with the same $300,000 annual expenses, about 21 years of runway

The underlying message is simple: if the asset appreciates faster than living costs, financial independence becomes more achievable over time.

But the volatility is real

The source does not dodge the hard part. Bitcoin is described as very volatile. That is the challenge.

But it is also framed as part of Bitcoin’s strength by people who have spent time studying the monetary system and hard money. In that worldview, volatility is not a side note. It is part of the reason the long-term thesis exists at all.

Why stopping at 0.1 Bitcoin is not the point

There is also a warning here: 0.1 Bitcoin matters, but it is not a finish line. The source pushes back against obsessing over fixed milestone numbers like 0.1, 0.21, or 0.5 as if they apply equally to everyone.

These figures are described as arbitrary markers. What matters more is personal context:

- Current income

- Expenses

- Financial goals

- Available means

Still, the argument is clear. Reaching 0.1 Bitcoin can be a meaningful first milestone because it starts building a foundation of reduced stress, increased leverage, and future optionality.

The strategy is slower than people want

If there is one theme running through the material, it is this: consistency beats intensity.

The source explicitly warns against going all in at once. A measured plan matters more than dramatic conviction. Dollar-cost averaging is presented as the practical path because it makes accumulation achievable over time.

Examples from the source

- $100 per month = $1,200 per year

- At a $70,000 Bitcoin price, that equals about 0.017 Bitcoin per year

- $10 per day = $3,650 per year

- At a $70,000 Bitcoin price, that equals about 0.05 Bitcoin per year

The material also gives a longer-range example: adding $100 a month on the path to 0.1 Bitcoin could, under the projection used, lead to 20 years of expenses covered by 2029, with a total fiat investment of $46,000 and a projected stack value of $5.79 million.

The numbers are ambitious. But the behavior being promoted is not: keep stacking, keep it realistic, and do not mistake entertainment for action.

Tracking matters more than hype

The article’s final practical point is almost old-fashioned: know your numbers.

Even higher-net-worth clients, the speaker says, often do not know their monthly expenses in granular detail. Without a budget, a cash-flow plan, and expense tracking, even the best Bitcoin plan turns fuzzy fast.

The bigger message is that 0.1 Bitcoin is not a substitute for financial organization. It works best as part of a broader structure.

What this really comes down to

The case for 0.1 Bitcoin is not built on instant riches. It is built on relief.

Relief from always being one problem away from panic. Relief from making every decision in survival mode. Relief that can eventually turn into leverage, better choices, and a stronger path toward financial independence.

That is why the source insists the idea is not hyperbole. Not because 0.1 Bitcoin changes everything tomorrow, but because for people living with constant financial strain, a real buffer can change life long before full financial freedom arrives.

FAQ

Is 0.1 Bitcoin supposed to make someone rich overnight?

No. The material is explicit about that. The argument is that 0.1 Bitcoin can reduce financial stress, create runway, and provide leverage—not instantly create massive wealth.

Why does 0.1 Bitcoin matter so much in this argument?

Because the source compares it to the financial reality of the average household. With median transaction savings at $8,000 and many people living paycheck to paycheck, a future value of $100,000 is presented as a serious buffer.

How could 0.1 Bitcoin reduce financial anxiety?

The claim is that a larger financial buffer changes decision-making. Instead of constantly reacting to bills and unexpected costs, people can think longer term and act with less panic.

Can 0.1 Bitcoin help someone leave a toxic job?

According to the material, yes—at least potentially. A stronger financial cushion can give someone time to leave a bad work situation and search for work that aligns better with their values.

Does the source say 0.1 Bitcoin is enough for full financial independence?

No. It says clearly that 0.1 Bitcoin will not fully make someone financially free. It is described as a meaningful milestone and a foundation, not the final destination.

What is the leverage advantage of holding Bitcoin?

The material argues that people may be able to borrow against Bitcoin without selling it. That means keeping exposure to appreciation while accessing capital, similar to strategies historically used by the wealthy.

What accumulation approach is recommended?

A gradual one. The source favors dollar-cost averaging over going all in, emphasizing that consistency beats intensity in the long run.

What is the biggest takeaway from the 0.1 Bitcoin thesis?

That a seemingly small amount can become meaningful when viewed through the lens of real household finances, long-term appreciation, and the emotional impact of having true financial runway.

Source

Omar Al-Sharif lives and works in the UAE and is involved in the blockchain technology industry. He writes articles on Bitcoin and digital assets as a personal passion, explaining complex topics in simple and understandable language.