For years, buying a home and holding Bitcoin felt like a brutal trade-off. Keep the asset you believe in, or sell it to chase stability. That tension may have just cracked open in a way a lot of people did not see coming.

Something bigger than a niche crypto product is taking shape here. The shift is not just about a mortgage. It is about whether Bitcoin is now being treated as real collateral inside the system that defines the American dream.

What just happened with Bitcoin-backed mortgages?

Fanny Mae, described here as a $4.5 trillion US government-backed institution, has approved a Bitcoin-backed mortgage structure through the mortgage loan process for the first time ever. That is the turning point driving so much attention.

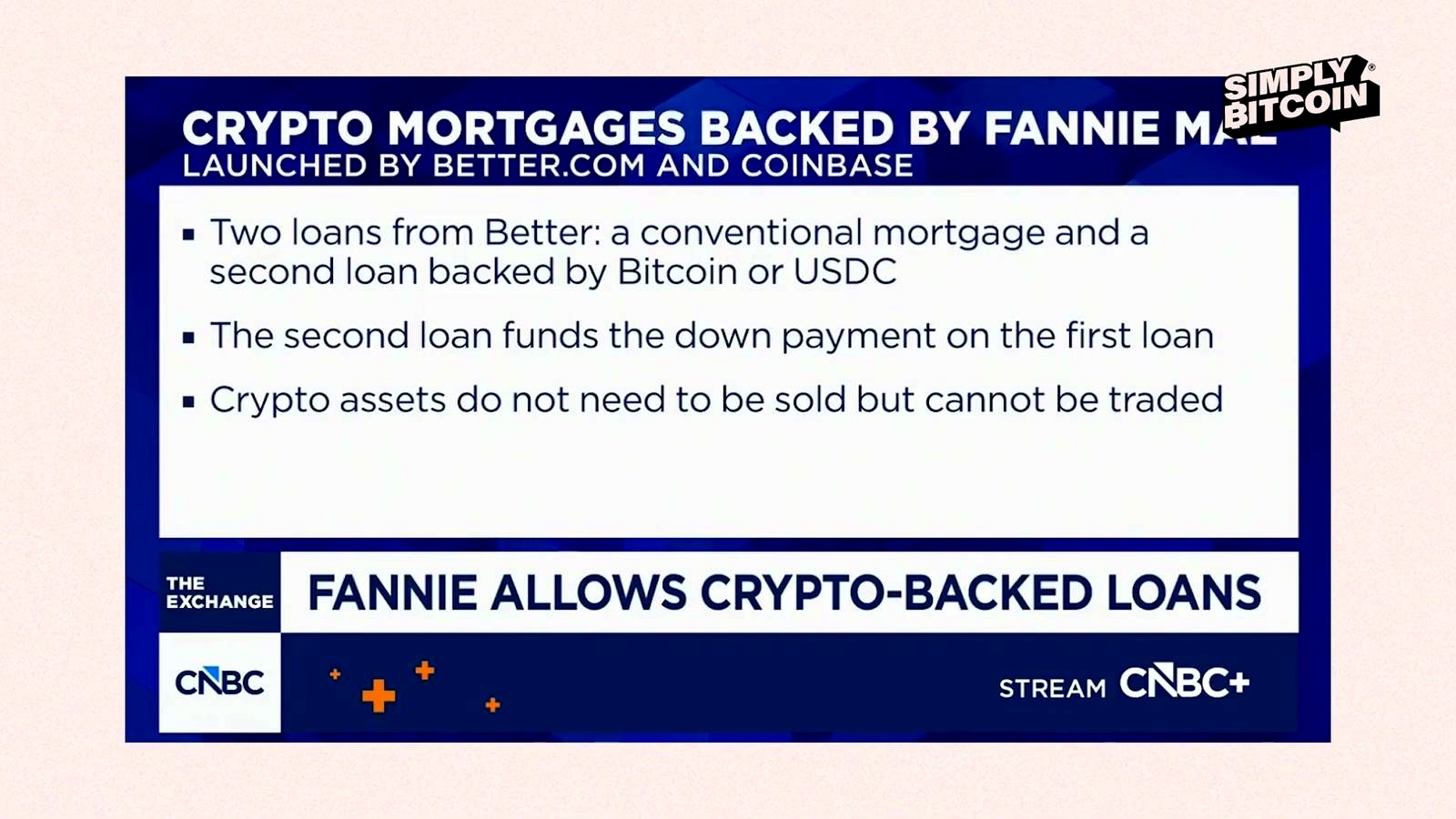

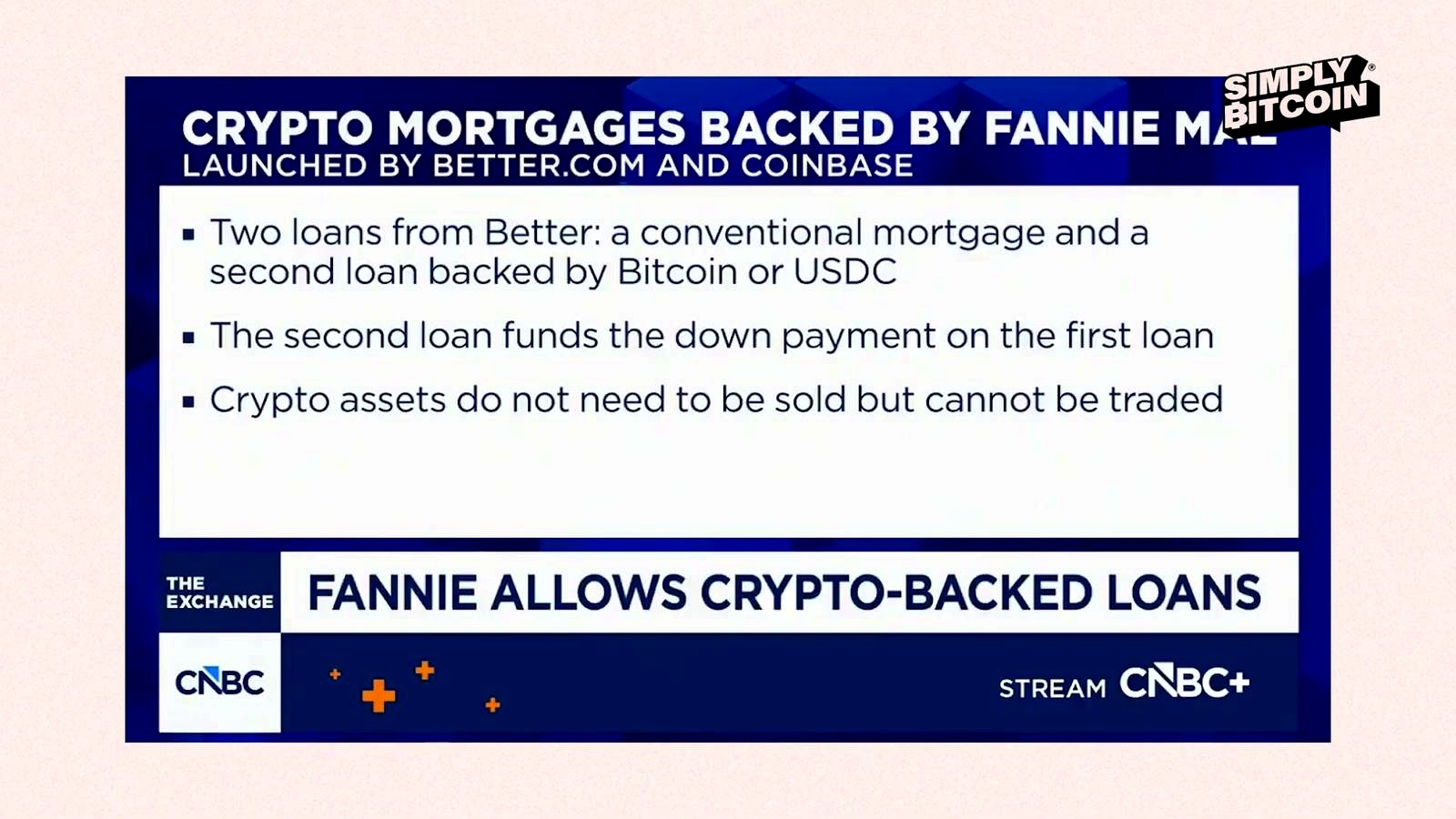

According to the material, this is not the first crypto-backed mortgage. But it is the first one built to comply with Fanny Mae requirements for purchase. That means it can be bought and securitized by Fanny Mae like other conforming mortgages.

Who is offering it?

Better Home and Finance, together with Coinbase, are offering the mortgage product. The idea is simple in spirit, even if the structure is more complex in practice: use crypto assets as collateral so a home buyer does not have to sell them.

How the Bitcoin-backed mortgage works

The setup uses two loans.

- The borrower takes out a regular mortgage with Better.

- The borrower also takes out a second loan backed by Bitcoin or USDC held in a Coinbase account.

That second loan funds the down payment on the first loan. The key outcome is what makes this feel so different: the borrower does not have to sell their crypto.

The important mechanics

- Both loans are held by Better.

- The pledged crypto assets cannot be traded once committed.

- If the value of the crypto falls, the loans do not change as long as monthly payments continue.

- The only liquidation risk mentioned is delinquency if no payments are made for 60 days or more, described as similar to a conventional mortgage.

That last point is doing a lot of work. In the material, this is framed as a major difference from the fear many people attach to crypto-backed borrowing.

Why this feels bigger than a mortgage product

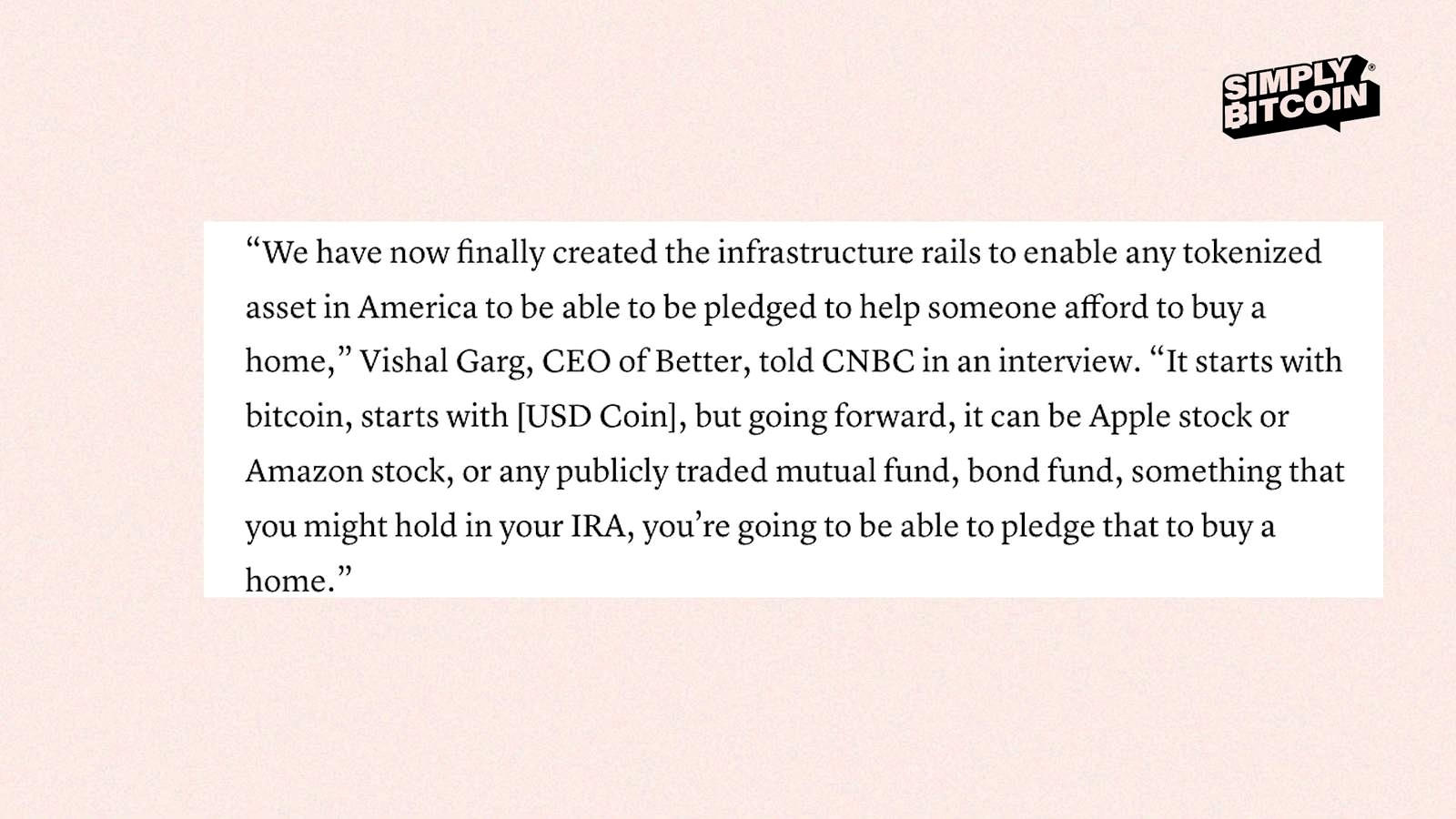

The article source frames this as a tactic long used by billionaires finally becoming available to ordinary people: borrow against assets, never sell. That has been the game for the wealthy for decades. Now, the same idea is being applied to Bitcoin holders trying to buy a home.

The emotional hook is obvious. People who spent years saving in Bitcoin, dealing with volatility, and delaying gratification have often faced the same ugly choice when life changes: sell the asset, trigger capital gains, and lose future upside. This structure is presented as a way around that.

The claimed advantages

- No forced liquidation just to fund a home purchase

- No capital gains tax event from selling Bitcoin for the down payment

- Continued exposure to Bitcoin if it appreciates

- Access to a conforming mortgage framework under Fanny Mae guidelines

The source says the rate is only 0.5% to 1.5% higher than a normal rate, though it also acknowledges the borrower is paying on two loans, making the arrangement more expensive.

The trade-off nobody should ignore

This is not being described as free money or some magical workaround. There is a downside stated plainly: two loans mean more cost.

The bullish argument in the material is that if the crypto appreciates, that appreciation could offset the added expense. But the core structure still asks the borrower to carry more financing. That makes this feel less like a loophole and more like a new financial tool with very specific logic behind it.

Why supporters still see it as worth it

The answer comes back to one idea again and again: you keep the Bitcoin. For supporters, that matters more than almost anything else. Selling means taxes, opportunity cost, and in the language of the source, the emotional toll of giving up “the only asset that you actually believed in.”

Why Bitcoin is being framed as “pristine collateral”

The material repeatedly calls Bitcoin a superior savings technology and even “the supreme pristine collateral asset.” That is the lens through which this mortgage announcement is being interpreted.

The broader claim is not merely that Bitcoin can be used in housing finance. It is that the system is beginning to validate Bitcoin as actual collateral.

The argument behind that view

Michael Saylor is quoted describing Bitcoin as pure monetary equity: liquid, portable, scarce, and global. The comparison drawn in the material is sharp. A house can come with roof repairs, plumbing issues, and property tax surprises. Bitcoin, in that framing, does not.

He also argues that if Bitcoin continues growing faster than the cost of mortgage debt, the Bitcoin-backed equity can outpace the debt burden itself. The source then pushes the idea further: homes priced in Bitcoin get cheaper over time.

Why supporters think this matters for the American dream

There is a direct housing affordability angle in the material. Federal Housing Finance Agency director Bill Pulte is quoted saying crypto has an enormous opportunity to help with the affordability equation, adding that many people have a lot of wealth in Bitcoin and should have access to the American dream.

That is the real emotional center of the story. Not “cool crypto mortgage.” Not even product innovation on its own. It is the idea that housing, savings, and investing may be rearranging around a different kind of asset.

The old model vs the new model

- Old model: work, save dollars, buy a house, benefit

- New model described here: save in Bitcoin, never sell it, borrow against it, and let appreciation support the debt structure

The source calls that a radically different world. One where everyday people have access to tools once reserved for the wealthy.

The wider theory behind the excitement

The mortgage story is being placed inside a much larger thesis. Jeff Park of ProCap Financial is cited arguing that every generation experiences a great monetary reset, and that the future will not look like the past.

That argument leans on demographic and structural changes described in the material:

- An aging population

- Fertility rates collapsing

- Household formation changing

- Debt burdens rising

- Inflation rising

- A shift from physically stored assets to digitally stored assets

Within that view, wealth could move toward digitally native assets, and the next generation may store economic energy in an asset rather than a home. In the source material, that asset is Bitcoin.

What critics are expected to say

The source openly anticipates backlash. It predicts critics will call the structure risky and warn that Bitcoin could lead to home liquidations.

There is also a direct argument against tokenized gold as the real competitor. The material claims gold cannot serve this role as effectively because banks do not want the burden of validating, storing, and managing physical gold collateral. Bitcoin, by contrast, is presented as much easier to verify and manage in a digital wallet.

Why that debate matters

This is really a fight over what kind of asset the financial system wants to work with. The source argues that if gold were better for this job, products would already have been built around it. Instead, the choice was Bitcoin.

Why this may be one of the biggest Bitcoin adoption stories yet

When supporters zoom out, they see a pattern. The material says Bitcoin is becoming the basis of ETFs, treasury reserve assets, sovereign conversations, and now mortgage collateral.

That is why this moment is being framed as more than another crypto headline. Once Bitcoin enters the machinery of mainstream housing finance, the symbolism changes. It starts to look less like an outsider asset and more like something the system can build on.

The final takeaway in the source is blunt: when the American government is effectively saying Bitcoin can help fund the American dream, people should pay attention.

FAQ

What is a Bitcoin-backed mortgage in this case?

It is a structure where a borrower takes a regular mortgage and a second loan backed by Bitcoin or USDC. The second loan is used for the down payment, so the borrower does not have to sell crypto.

Does the borrower have to sell Bitcoin to buy the house?

No. The central point of the product is that the borrower can pledge Bitcoin as collateral instead of selling it.

Who is offering the mortgage product?

Better Home and Finance and Coinbase are named as the companies offering this mortgage structure.

Why is Fanny Mae’s role important?

Because this product is described as the first crypto-backed mortgage to comply with Fanny Mae requirements for purchase, allowing it to be bought and securitized like other conforming mortgages.

What happens if Bitcoin falls in value?

According to the material, nothing changes on the loans as long as the borrower keeps making monthly payments.

Can the pledged crypto still be traded?

No. Once the crypto assets are pledged, they cannot be traded.

What is the main downside?

The borrower is paying on two loans, which makes the arrangement more expensive.

Why are supporters calling this a game changer?

Because they see it as bringing a long-used wealth strategy to ordinary people: borrow against assets, avoid selling, and keep exposure to future appreciation.

Original Video

Omar Al-Sharif lives and works in the UAE and is involved in the blockchain technology industry. He writes articles on Bitcoin and digital assets as a personal passion, explaining complex topics in simple and understandable language.