What does it mean when Michael Saylor stops buying Bitcoin after 13 straight weeks? That was the key tension raised by MSTR & the Treasury Titans, which framed the pause not as a retreat, but as part of a broader bet on Bitcoin-backed financial products.

According to MSTR & the Treasury Titans, Strategy’s decision to make no new Bitcoin purchase last week may have less to do with fading conviction and more to do with cash management around dividend obligations tied to its preferred instruments. The host argued that the lack of a buy announcement ended a notable run, but did not change his bullish stance on Bitcoin, MSTR, or the company’s expanding “digital credit” pitch.

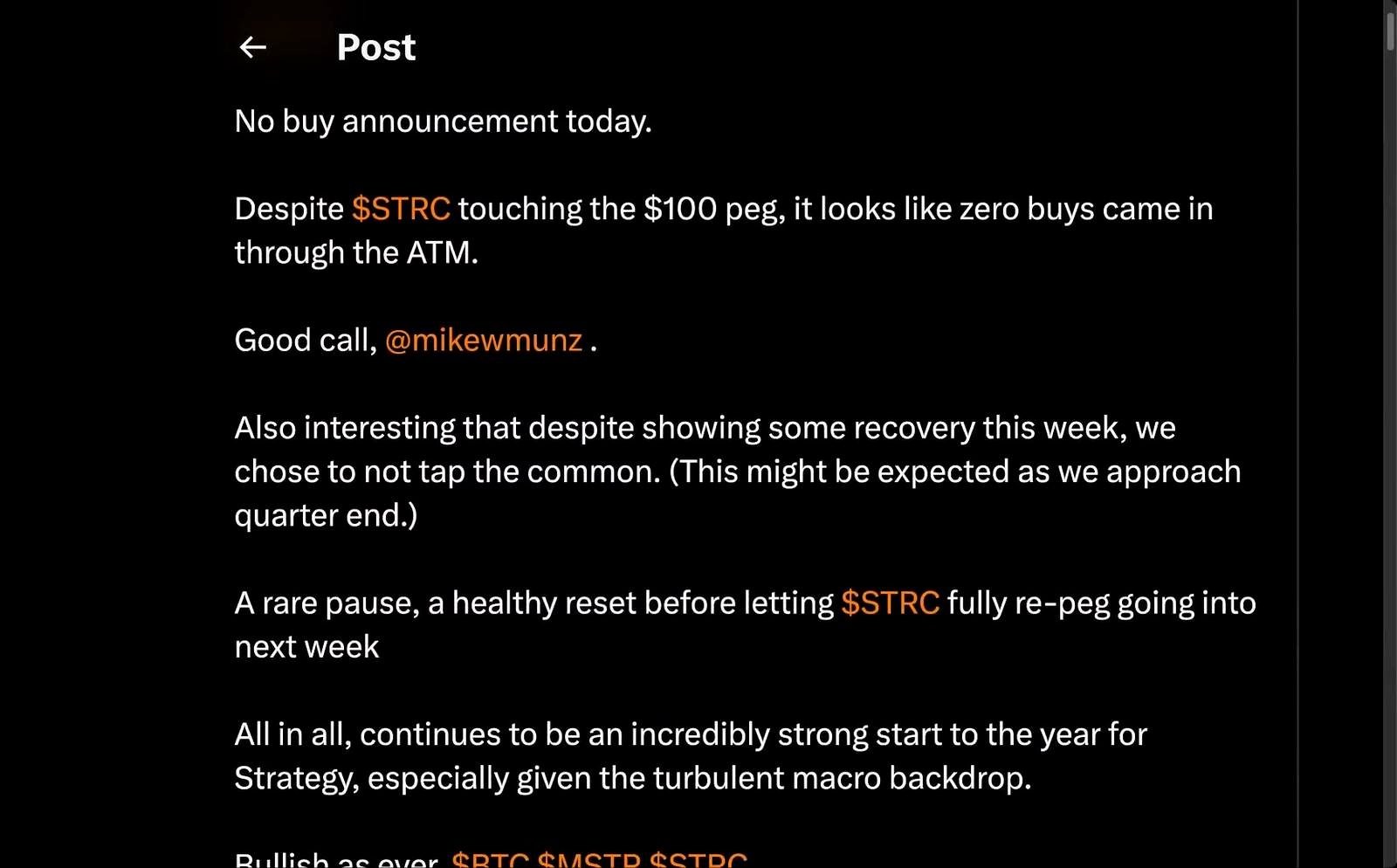

The headline: no Bitcoin buy after 13 straight weeks

The clearest news point from the video was simple: Strategy appears to have paused Bitcoin accumulation for the first time in 13 weeks. The host cited a CoinDesk report saying the streak included more than 90,000 BTC acquired since late December.

That break matters because Strategy’s Bitcoin purchases have become a closely watched signal for the market and for MSTR holders. But the host did not treat the pause as a bearish turn. Instead, he suggested the company may have redirected cash raised through its at-the-market program to cover dividends rather than buy more BTC immediately.

That explanation was explicitly framed as interpretation, not confirmed fact. The host said he was “reading in the tea leaves” and expected more clarity when a later filing appears.

The working theory: dividend payments may have taken priority

According to MSTR & the Treasury Titans, the most plausible reason for the no-buy week is that Strategy needed liquidity for dividend payments linked to products the host referred to as “stride” and “stretch.” He said he believed the company may have tapped MSTR’s ATM during the week and then held the proceeds in cash instead of deploying them into Bitcoin.

The host’s case rests on timing. He pointed to an upcoming dividend cycle and said investors may be positioning around an ex-dividend date he believed was either the next day or the day after, with another ex-dividend date on April 15. In his telling, that creates a near-term setup where capital chases the yield product first, then rotates back toward MSTR exposure.

He also argued Strategy would prefer not to draw down existing cash reserves if those reserves are intended to remain intact or grow. That is why, in his view, temporarily pausing Bitcoin purchases would be acceptable during a choppy market.

The numbers the host focused on

The video included a dense set of figures tied to Strategy, Bitcoin, MSTR, and the firm’s preferred products. Here are the specific numbers mentioned:

- Strategy and affiliated holdings: over 760,000 BTC

- Buying streak ended after 13 weeks

- BTC acquired during that streak: over 90,000 BTC

- MSTR pre-market price cited: $99.97

- MSTR pre-market volume cited: over 450,000

- Expected positioning window: 10 to 11 trading days

- Next ex-dividend date mentioned: April 15

- Host’s estimate for one yield product: 11.5%

- Host’s estimate for another yield product: 13.5%

- Tax deferral period referenced: 9-plus years

- BTC price dip and rebound cited: from $65,000 to over $67,000

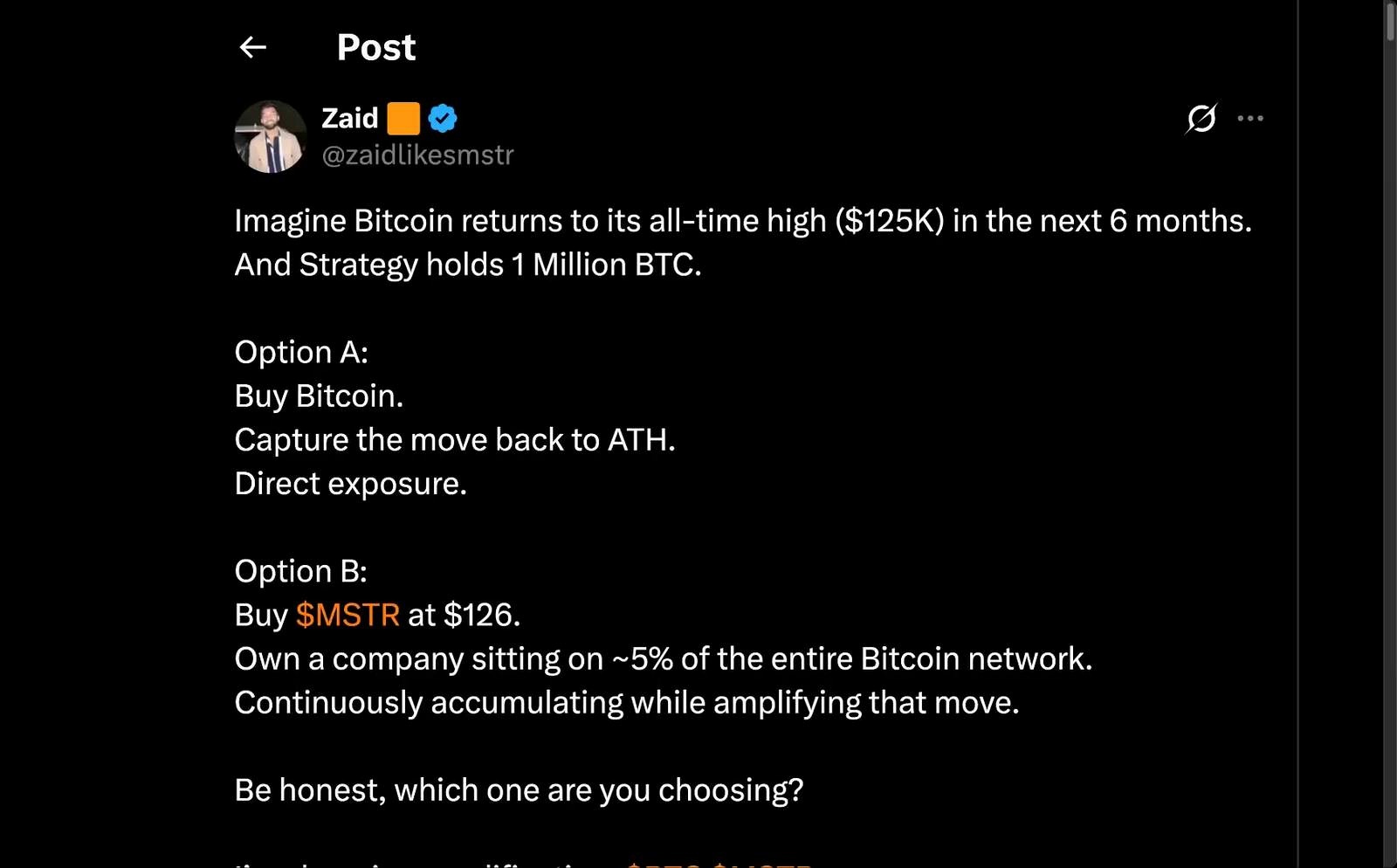

- BTC all-time high referenced by a commenter: $125,000 within 6 months

- Hypothetical Strategy holdings: 1 million BTC

- Hypothetical MSTR buy point: $126

- Claimed share of Bitcoin network at 1 million BTC: 5%

- Host’s comment on BTC’s biggest yearly moves: 10 to 15 days a year

- Market move comparison from a commenter: down 10%, then up 20%

- BTC level cited for April in that example: $76,000

- BTC peak cited for October in that example: $126,000

- Year for new all-time highs prediction: 2026

- Bitcoin ARR figure cited by the host: 2.13%

- Incorrect range he criticized in another video: 20% to 30%

- Longevity estimate at 0% growth: over 70 years or 50 years

- Alternative volatility/return figures discussed: 30% ARR and 52% ARR

- Host’s holding horizon: 3, 7, and 12 years

- Private credit market size cited by Michael Saylor clip: $3.7 trillion

- Typical private credit return cited: 10% or 11%

- Example diversification reference: 1,000 projects or companies

- Example loan duration: 5-year loans

- Northwest Registered Agent operating history in ad read: nearly 30 years

- Corporate guides cited in ad read: over 1,500

The bigger thesis: “digital credit” versus private credit

The most developed argument in the video was not the no-buy week itself. It was the claim that Bitcoin-backed “digital credit” could outcompete traditional private credit.

According to MSTR & the Treasury Titans, Michael Saylor’s core pitch is that digital financial products built on Bitcoin can combine features that investors usually cannot get in one instrument: double-digit returns, tax deferral, lower volatility, and principal protection. The host said that is why he views products like “stretch” as central to the broader Strategy story.

To reinforce that point, he played a Saylor clip contrasting digital credit with private credit. In that clip, Saylor described private credit as illiquid, opaque, heterogeneous, restricted, and fee-heavy. He then contrasted it with digital credit, which he called liquid, transparent, homogeneous, scalable, accessible, and fee-free.

Saylor also put a market size on the opportunity, saying private credit is a $3.7 trillion market and arguing that its main weaknesses are illiquidity and heterogeneity. His conclusion was that Bitcoin-backed collateral solves both problems in a novel way.

Why the host thinks the setup is still bullish

Even with no fresh Bitcoin purchase, the host stayed firmly bullish. He argued that the market is overly bearish at a moment when Bitcoin could still move sharply higher, and he said he wants exposure because Bitcoin’s most powerful gains often come in a small number of sessions each year.

He also embraced the idea that MSTR can offer leveraged or “amplified” exposure compared with holding BTC directly, especially if Strategy keeps accumulating and if Bitcoin revisits higher price levels. One commenter he quoted sketched a scenario where Bitcoin returns to $125,000 within 6 months and Strategy reaches 1 million BTC. The host did not present that as a firm forecast, but he clearly favored the amplification argument behind owning MSTR.

He also pushed back on criticism of Strategy’s yield products, saying the relevant Bitcoin ARR is 2.13%, not 20% to 30%. In his framing, that lower figure means the dividend can be sustained indefinitely. He went further, saying that even at 0%, the timeline before the structure would need rethinking could run 50 to 70-plus years, though he attributed that rough point to prior comments from Saylor.

What to watch next

The next thing to watch is not a grand macro event. It is confirmation. If a later filing shows Strategy raised capital but did not deploy it into Bitcoin, that would support the host’s dividend-funding theory. If the filing shows otherwise, the no-buy week may need a different explanation.

Beyond that, the key near-term marker in the video was April 15, which the host identified as the next ex-dividend date for one of Strategy’s products. The broader issue is whether these instruments deepen investor demand for Strategy equity and preferreds without interrupting the company’s Bitcoin accumulation strategy for long.

For now, the host’s position is straightforward: a pause in weekly buying does not weaken the long-term thesis. In his view, it may simply show that Strategy is trying to build something larger than a corporate Bitcoin treasury, a Bitcoin-backed capital stack.

FAQ

Did the video say Strategy is turning bearish on Bitcoin?

No. The host treated the no-buy week as a tactical pause, not a shift in conviction. He remained openly bullish on both Bitcoin and MSTR.

Was there any confirmed reason given for the lack of a Bitcoin purchase?

No confirmed reason was provided in the transcript. The host’s main explanation was that cash may have been held back to pay dividends tied to Strategy-linked products.

What is the core argument for “digital credit” in this video?

The pitch is that Bitcoin-backed credit instruments could offer yields comparable to private credit while improving liquidity, transparency, standardization, and accessibility.

Why did the host criticize other commentary on Strategy’s products?

He argued that some critics are using the wrong assumptions, especially around Bitcoin ARR. His claim was that a 2.13% figure makes the structure far more durable than commentators suggesting 20% to 30%.

What was the most important date mentioned?

April 15. The host pointed to that ex-dividend date as the next checkpoint for investor flows and for judging whether demand is building around Strategy’s preferred instruments.

Source

An Indian crypto journalist covering the developments in the Bitcoin and blockchain industries. Her work helps readers understand key changes in the world of digital assets.