Risk assets are trading between relief and fragility. A ceasefire narrative briefly pushed Bitcoin toward a breakout, but the move faded fast, leaving traders to ask whether institutional demand is still strong enough to carry BTC higher through geopolitical and macro noise.

According to FireHustle, the more important story is not the short-term pullback but the speed of Wall Street’s product buildout around Bitcoin, especially Goldman Sachs’ new income-focused ETF filing and what it signals about the next class of buyers.

The Core Thesis: Wall Street Is Moving From Bitcoin Access to Bitcoin Packaging

According to FireHustle, Goldman Sachs’ filing for a Bitcoin premium income ETF marks a new phase in institutional crypto adoption. The host’s central argument is that the market has moved beyond the question of whether major firms will offer spot Bitcoin exposure. Now the competition is over how many kinds of Bitcoin-linked products banks can package for different client bases.

The filing, submitted on April 14, describes a fund that would not hold Bitcoin directly. Instead, it would gain exposure through existing spot Bitcoin ETFs and options tied to those products. FireHustle said the strategy would sell call options on roughly 40% to 100% of the fund’s Bitcoin exposure, depending on conditions, with the option premiums distributed to investors as income. The trade-off is straightforward: investors get cash flow, but upside is capped if Bitcoin rallies sharply.

That framing matters because it broadens the addressable market. Spot ETFs solved the access problem for institutions and advisers. Covered-call Bitcoin funds target a different audience altogether: retirees, wealth managers, income mandates, and portfolios that want crypto exposure without taking full directional volatility. FireHustle argues this could create a new layer of structural demand.

In broader market context, that is a plausible but not uncontested thesis. Covered-call funds tend to attract conservative capital, and in traditional markets they are often sold as lower-volatility income vehicles. But with Bitcoin, the underlying asset is far more volatile than blue-chip equities, and call overwriting can materially reduce upside in the very scenarios that make many allocators interested in BTC in the first place. Still, the strategic shift is real: major issuers are no longer merely launching plain-vanilla Bitcoin products. They are segmenting the market.

Why the Filing Stands Out

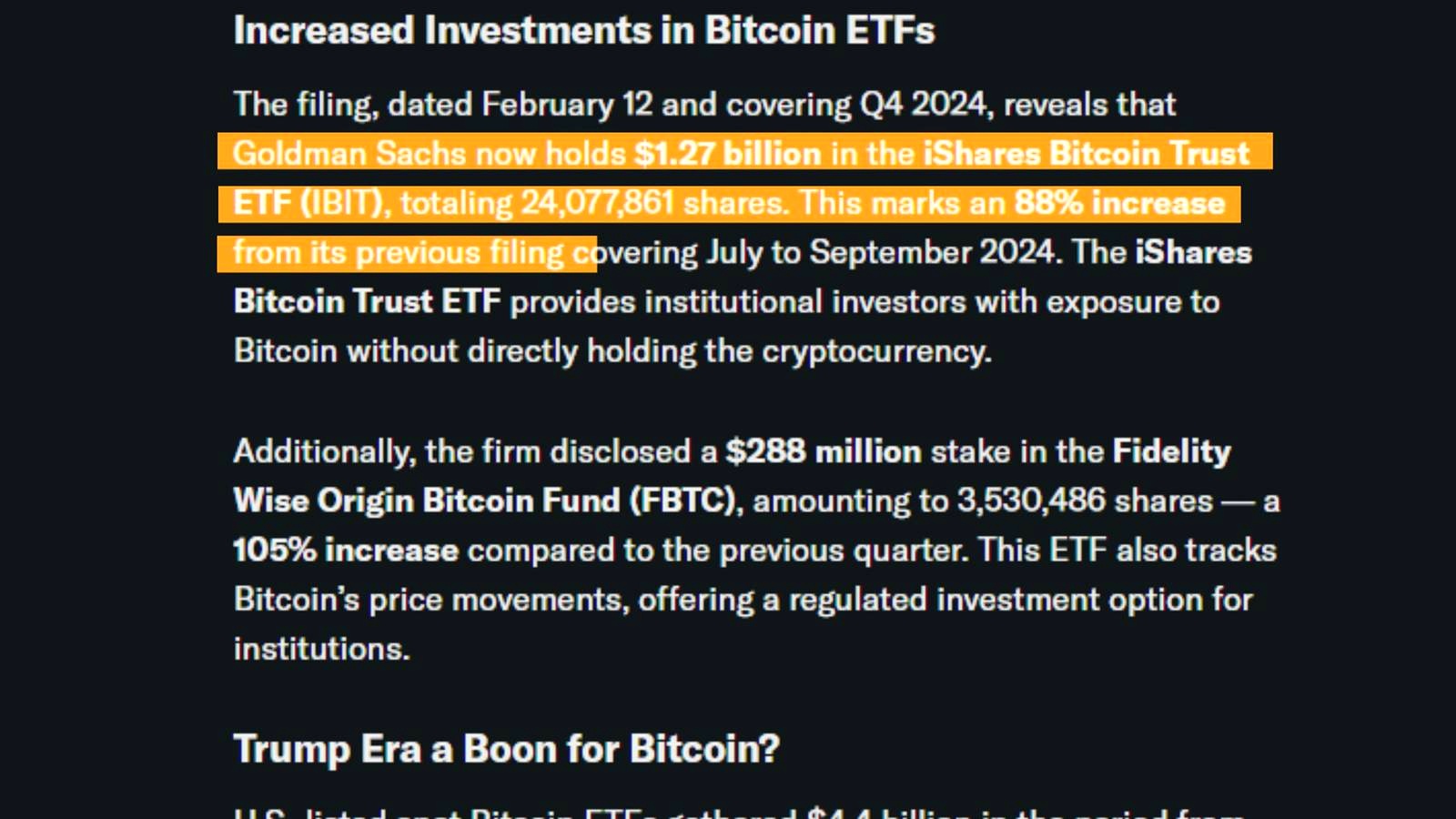

According to FireHustle, the reason this is bigger than “just another ETF” is the institutional weight behind it. The host said Goldman Sachs manages roughly $3.6 trillion in assets and had previously disclosed around $1.27 billion in the iShares Bitcoin Trust, an 88% increase from the prior quarter. In FireHustle’s reading, that suggests Goldman was already building exposure before deciding to put its own brand directly on a Bitcoin product.

The timing also matters. FireHustle linked Goldman’s filing to a broader competitive push across Wall Street. BlackRock, he said, updated an S-1 on April 1 for its own Bitcoin premium income ETF under the ticker BITA. Morgan Stanley, meanwhile, launched its spot Bitcoin ETF, MSBT, on April 8, with an annual fee of 0.14%. FireHustle said that product drew $34 million in first-day inflows and traded more than 1.6 million shares.

That sequence supports the host’s “arms race” framing. Fees are being compressed, product types are multiplying, and brand-name institutions are targeting separate investor cohorts rather than fighting for a single spot-ETF buyer. In mature asset classes, that is usually what happens after an initial adoption wave proves demand exists.

FireHustle also tied the story to fresh market inflows. He said spot Bitcoin ETFs saw $411 million in inflows the day after Goldman’s filing became public, bringing total assets under management across spot products to $96.5 billion. He also cited cumulative inflows of more than $56 billion across spot Bitcoin products and nearly $64 billion in net inflows into BlackRock’s IBIT since launch.

Even without taking every bullish implication at face value, the direction is clear: Bitcoin financialization is accelerating. That tends to deepen liquidity, improve access, and pull in more traditional allocators. It can also make BTC more sensitive to the mechanics of options markets, fund flows, and macro positioning.

Price Action, Macro Tension, and the Near-Term Setup

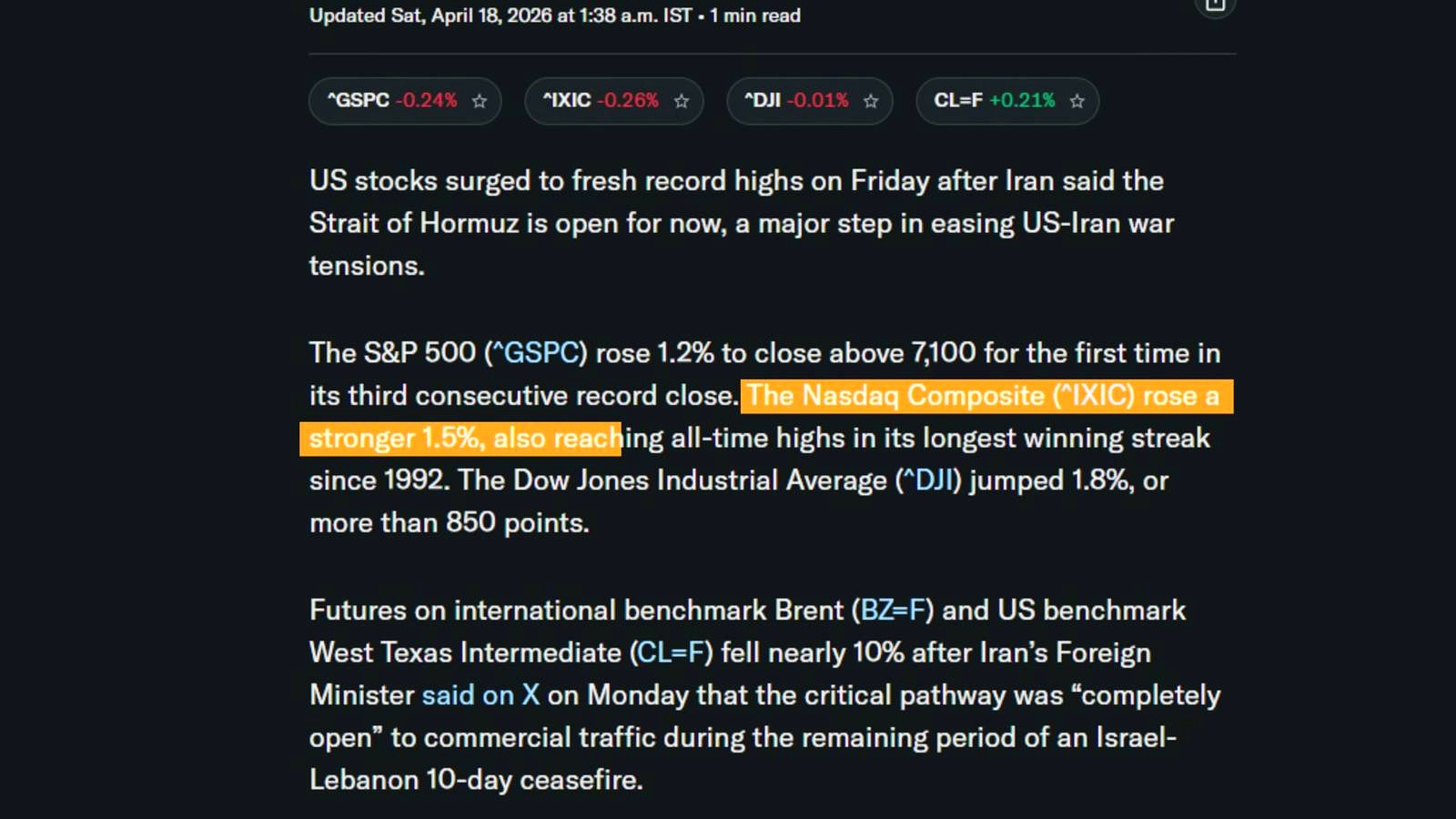

According to FireHustle, Bitcoin nearly touched $78,000 over the last 7 days as optimism around a US-Iran ceasefire pushed risk assets higher. The host said the Nasdaq closed at session highs with a 2% gain, while oil fell below $93 a barrel. For a moment, he argued, markets looked ready to break out of a 2-month consolidation.

But the move failed. FireHustle said Bitcoin slipped back below $74,000 by the end of the session, with profit-taking driving prices down almost 3% by Wednesday. At the time of the video, BTC was trading around $75,000 to $76,000.

The analyst’s point here is less about a tactical trade than about the disconnect between shaky retail sentiment and steady infrastructure growth. He highlighted Strategy’s purchase of 13,927 BTC for roughly $1 billion at an average price of $71,900, pushing its holdings above 780,000 BTC worth nearly $59 billion. He also said Tether added $70 million in Bitcoin, taking its reserves past 97,000 BTC.

That combination, hesitant price action alongside continued treasury and ETF accumulation, is one of the more important tensions in the current market. Bulls see it as absorption: weak hands sell into every rally, while institutions keep buying the asset and the wrappers around it. Bears see a different story: more product supply does not guarantee immediate spot demand, especially if rates stay high and geopolitical risk keeps inflation expectations elevated.

FireHustle flagged both themes. He noted that rate cuts are “not coming anytime soon, ” while also warning that a supply shock linked to the Strait of Hormuz had not fully hit markets yet. If energy prices rebound, the macro backdrop for Bitcoin could become more complicated, even with strong ETF demand.

What Could Go Wrong

The biggest risk to FireHustle’s thesis is that investors may overstate what covered-call Bitcoin products actually do for BTC price. These funds are bullish for market infrastructure and adoption, but they are not pure upside vehicles. By design, they monetize volatility and cap part of the upside. If a large portion of incoming capital chooses income-oriented products instead of outright spot exposure, the result could be steadier but less explosive participation.

There is also a macro problem. FireHustle emphasized the ceasefire and falling oil as a tailwind, but he also acknowledged that the geopolitical picture remains fragile. If peace talks stall further, if energy markets tighten, or if inflation expectations rise into the April 28 FOMC meeting, risk assets could reprice lower. Bitcoin has increasingly traded as a macro-sensitive asset during periods of rate uncertainty, not as a clean hedge against them.

Another weak point is regulatory timing. FireHustle said Goldman’s filing implies a 75-day effectiveness window, pointing to a possible launch in late June or early July. But ETF review timelines can slip, and politically favorable crypto messaging does not guarantee smooth approvals for every product structure.

Finally, product proliferation cuts both ways. More Wall Street involvement brings more liquidity and more legitimacy. It also means more derivatives, more structured exposure, and more pathways for traditional finance to dampen or reshape Bitcoin’s price behavior. That is bullish for adoption, but not always in the way cycle traders expect.

What to Watch Next

The first near-term trigger is the April 28 FOMC meeting, which FireHustle said could set the tone for risk assets into the summer. Traders will also be watching whether oil stays below $93 or reverses higher on renewed Middle East stress.

On Bitcoin itself, the practical levels are the failed breakout near $78,000, the pullback zone around $75,000 to $76,000, and the loss of momentum below $74,000. On the structural side, late June to early July is the key window if Goldman’s income ETF moves through review. Confirmation of similar launches from BlackRock would strengthen FireHustle’s broader claim that Bitcoin is entering a full-scale product expansion cycle.

FAQ

What is a covered-call Bitcoin ETF?

A covered-call Bitcoin ETF typically holds Bitcoin exposure, directly or through other funds, and sells call options against that exposure. The option premiums generate income, but the strategy gives up some upside if Bitcoin rallies above the strike price.

How is a Bitcoin income ETF different from a spot Bitcoin ETF?

A spot Bitcoin ETF is mainly designed to track Bitcoin’s price. A Bitcoin income ETF adds an options strategy on top of that exposure to generate regular premium income. In exchange, investors usually accept capped gains during strong rallies.

Why would retirees or wealth managers prefer this structure?

Many traditional portfolios are built around income and volatility control rather than maximum upside. A covered-call structure can make Bitcoin easier to sell to clients who want exposure to the asset class but are uncomfortable with its full price swings.

Does more ETF product variety usually help an asset class?

Often, yes. More wrappers can attract more investor types, improve access, and deepen liquidity. But the effect on price depends on the product mix. Vehicles that hedge or cap upside can support adoption without necessarily producing the same directional impact as outright spot buying.

What happened the last time Bitcoin failed near a breakout level?

Historically, failed breakouts in Bitcoin often lead to either a fast retest of support or a longer consolidation before the next impulse move. The key difference-maker is usually whether spot demand, ETF inflows, and macro conditions stay aligned during the pullback.

Original Source

An Indian crypto journalist covering the developments in the Bitcoin and blockchain industries. Her work helps readers understand key changes in the world of digital assets.