Something fundamental has shifted, and it’s not subtle anymore. The version of Bitcoin many investors thought they owned may be gone, replaced by an asset that now moves through the same macro storm as everything else.

That change matters most when markets are under pressure. Because when stocks slide, debt climbs, and liquidity drives the conversation, Bitcoin is no longer standing off to the side.

Bitcoin’s biggest change is hiding in plain sight

For most of its early life, Bitcoin was easy to dismiss as a sideshow. It lived in its own corner of finance, moving on its own terms and paying little attention to the S&P 500, bonds, oil, or gold.

That independence was a major part of its appeal. From 2015 through 2019, Bitcoin’s correlations with major asset classes hovered close to zero. Against the S&P 500, it barely registered, sitting around 0.03 to 0.05. Bonds, oil, and gold told a similarly flat story.

At that stage, Bitcoin looked like a genuinely separate asset. It was volatile and niche, largely held by retail speculators and idealists who were not plugged into broader market cycles. When equities rallied or sold off, Bitcoin often just shrugged.

Why that mattered so much

An asset that moves independently of everything else is powerful in a portfolio. Its value is not only about whether it rises or falls, but whether it behaves differently from the rest.

- It can reduce overall portfolio risk

- It offers diversification regardless of short-term direction

- It gives investors exposure to something outside traditional market behavior

That was the old argument for holding Bitcoin. And for a long time, it was compelling.

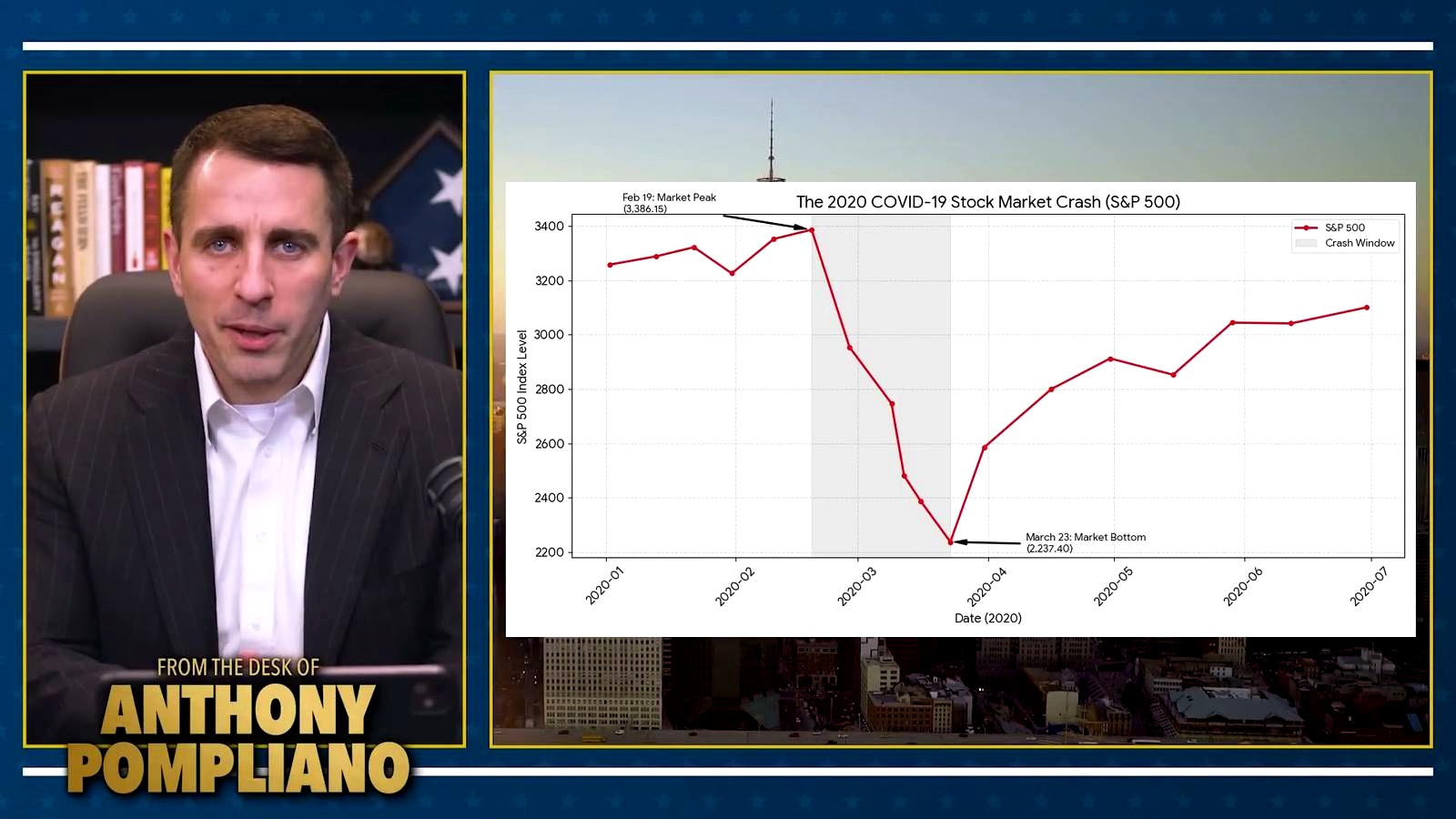

The pandemic broke the spell

The turning point came in March 2020. When markets crashed, Bitcoin was pulled into the same liquidation wave that hit equities, commodities, and credit.

Investors needed cash. They sold what they could sell. Bitcoin was liquid, so it was sold too.

Its correlation with the S&P 500 jumped from near zero to about 0.47 almost overnight. Then came the next phase: central banks flooded the system with liquidity, markets rebounded, and Bitcoin surged higher.

But this time, it did not surge alone.

It moved in lockstep with the tech-heavy NASDAQ and broader risk-on equities. The correlation with SPY kept climbing and eventually reached roughly 0.55 to 0.65 between 2021 and 2022.

What Bitcoin became

By then, Bitcoin had been absorbed into the macro trade. It was no longer behaving like a separate asset class. It had evolved into a high-beta expression of risk-on sentiment.

That shift reflected a deeper change: a different type of investor was now holding the asset. And that changed how it traded.

The ETF moment came with a cost

The approval of spot Bitcoin ETFs in January 2024 felt like a watershed moment. It was the kind of milestone that Bitcoiners and Wall Street institutions had once viewed as nearly unthinkable.

But the celebration came with a tradeoff.

Institutional capital flooded in, and with it came traditional Wall Street thinking. Portfolio managers running models and allocating across asset classes now owned Bitcoin too. That meant when they sold equities, they often sold Bitcoin as well.

The old idealist culture lost ground to more mechanical, more tactical capital. The result was a new reality: the differences in trading behavior between Bitcoin and other major assets began to fade.

Where the correlation stands now

Today, the Bitcoin-SPY correlation sits around 0.49, similar to where it ended last year. During volatile stretches, rolling short-term correlations have spiked as high as 0.88.

That is a very different world from the one Bitcoin once occupied.

Whatever investors may want to believe, the asset is now trading like a true risk asset. Anyone who bought it expecting it to zig when stocks zagged has had to confront the opposite outcome.

Bonds and oil tell a weaker story

Not every relationship has intensified. In fact, some remain almost too weak to matter.

Bitcoin and bonds

Using TLT as the reference point, Bitcoin’s correlation with long-duration Treasury bonds has stayed close to zero throughout its history. It used to sit around 0.01, and that is roughly where it sits today.

Bitcoin is risk-on. Bonds are risk-off. But the relationship is inconsistent and weak, making it difficult to use strategically.

Bitcoin and oil

Oil has followed a similar pattern. A 10-year Binance Research study found no significant long-term relationship between Bitcoin and crude prices.

Short-term spikes do happen, but they tend to snap back. The long-run correlation remains around 0.15, weak enough to be effectively meaningless.

The gold relationship is where things got strange

For years, Bitcoin carried a small positive correlation with gold, usually around 0.1 to 0.35. That supported the digital gold narrative and the idea that both assets responded to dollar weakness and inflation fears.

That relationship has now fallen apart.

Gold surged higher as a geopolitical safe haven last year while Bitcoin sold off. The two assets moved in almost opposite directions, creating one of the rare periods in history when these two store-of-value assets showed a negative correlation.

And it did not stop there.

This year, the Bitcoin-gold correlation has dropped to negative 0.69, the sharpest divergence on record. Since the February 20 bombing of Iran, gold has been selling off while Bitcoin has been appreciating. Even with the direction of travel switching, the negative correlation has remained persistent.

Why this matters

This is more than a chart oddity. It cuts straight into one of Bitcoin’s longest-running narratives.

- The digital gold story has weakened

- Gold and Bitcoin are no longer moving as if they share the same role

- Bitcoin is acting less like a safe haven and more like a macro-sensitive risk asset

Mass adoption changed Bitcoin itself

The takeaway is difficult but clear: Bitcoin has grown up, and that growth has changed it.

Larger pools of capital have adopted the asset. This new investor base does not treat Bitcoin as a renegade exception. It pulls Bitcoin into the same risk-on, risk-off regime it uses for everything else.

That means Bitcoin is now more integrated with the financial system and more responsive to macro conditions. It also means Bitcoin is considerably less useful as a diversifier than it once was.

Whether that is a feature or a bug depends on what an investor wanted Bitcoin to be in the first place.

The emotional break for early believers

There will always be hardcore Bitcoin believers who refuse to sell regardless of market conditions. But there is a growing sense that some of the selling from OG holders last year came from a harder realization.

The renegade asset they once bet everything on may be gone.

What remains is a slightly more volatile digital currency that hopes to keep attracting capital and outperforming the stock market, but to do so with much higher correlation to traditional risk assets.

Why macro now matters more than ever

If Bitcoin trades more like a macro asset, then understanding macro becomes unavoidable.

And right now, the backdrop is tense.

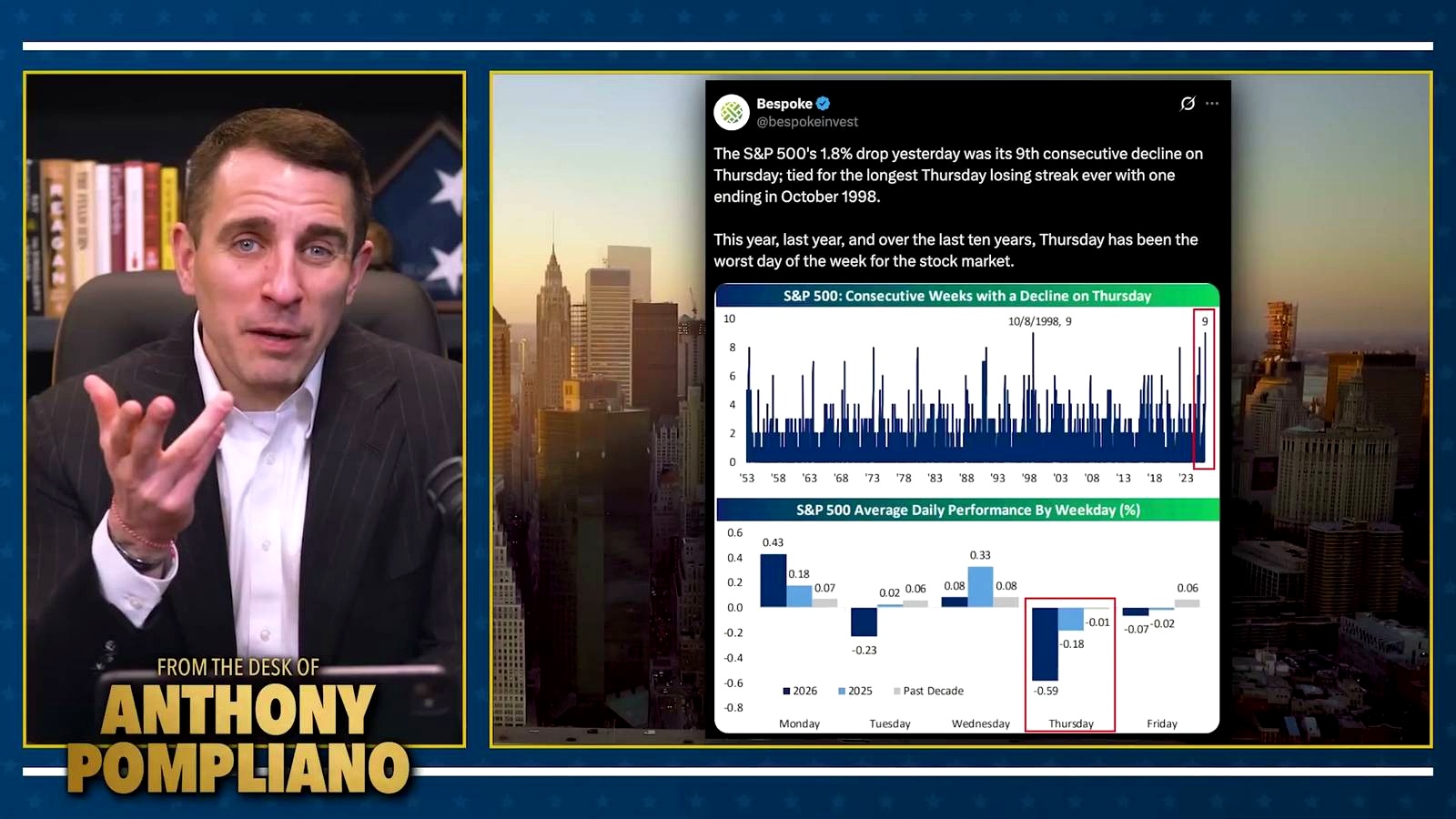

The stock market has been falling. The S&P 500 dropped 1.8% in a single day, marking the ninth consecutive Thursday decline. That ties the longest Thursday losing streak ever, matching one that ended in October 1998.

Notably, Thursday has been the worst day of the week for the stock market this year, last year, and over the last 10 years. When Thursday arrives, the data says investors should brace for impact.

The larger force underneath it all

Over long periods, the stock market has kept moving up and to the right. The argument here is simple: the national debt keeps rising, regardless of who is in the White House.

The next stop, according to this view, is a $40 trillion US national debt. If debt keeps rising, the dollar keeps getting debased. And if the dollar keeps getting debased, liquidity remains the force that matters.

That is why the stock market ultimately responds to liquidity conditions. And if Bitcoin now trades inside that same system, then Bitcoin investors need to understand those conditions too.

The slogan may as well be simple: regardless of party, print baby print.

What investors need to understand now

- Bitcoin is no longer behaving like a truly separate asset class

- Its correlation with stocks has become much stronger since 2020

- Institutional adoption and spot Bitcoin ETFs accelerated that shift

- Bonds and oil remain weakly connected to Bitcoin

- Bitcoin’s relationship with gold has turned sharply negative

- Macroeconomics and risk-on, risk-off regimes now matter much more for Bitcoin holders

That does not mean the opportunity is gone. It means the rules changed.

FAQ

Why is Bitcoin more correlated with stocks now?

Because larger pools of institutional capital now hold Bitcoin, and those investors often manage it alongside other assets. When they rebalance or reduce risk, Bitcoin can be sold with equities.

Was Bitcoin always supposed to be uncorrelated?

For much of its early history, it largely was. From 2015 through 2019, its correlations with major asset classes stayed close to zero, which made it attractive as a diversifier.

What changed in 2020 for Bitcoin correlations?

The March 2020 market crash pulled Bitcoin into a broad liquidation wave. After that, its behavior increasingly aligned with risk-on assets, especially as liquidity returned to markets.

How did spot Bitcoin ETFs affect Bitcoin trading behavior?

The approval of spot Bitcoin ETFs in January 2024 brought in more institutional capital and more traditional portfolio management behavior, which increased Bitcoin’s integration with the wider financial system.

Does Bitcoin still behave like digital gold?

The relationship with gold has weakened dramatically. This year, the Bitcoin-gold correlation fell to negative 0.69, marking a sharp divergence from the old digital gold narrative.

Is Bitcoin still useful for diversification?

It is considerably less useful as a diversifier than it once was, because it now trades more like a macro-sensitive risk asset with stronger correlation to stocks.

What should Bitcoin investors focus on now?

They need to better understand macroeconomics, liquidity conditions, and risk-on, risk-off regimes, because those forces now play a bigger role in where Bitcoin goes next.

Video Source

An Indian crypto journalist covering the developments in the Bitcoin and blockchain industries. Her work helps readers understand key changes in the world of digital assets.