Rising Bitcoin prices are supposed to revive mining economics, but for many retail participants the math still looks punishing. That tension sits at the center of a new VoskCoin video, which argues that even as BTC’s rally lifts miner revenue, the combination of thin hardware returns and questionable cloud-mining offers could leave smaller users exposed.

The Core Thesis

According to VoskCoin, the retail Bitcoin mining business looks increasingly unattractive unless an operator has unusually cheap power, and that makes high-yield cloud-mining pitches even more suspect.

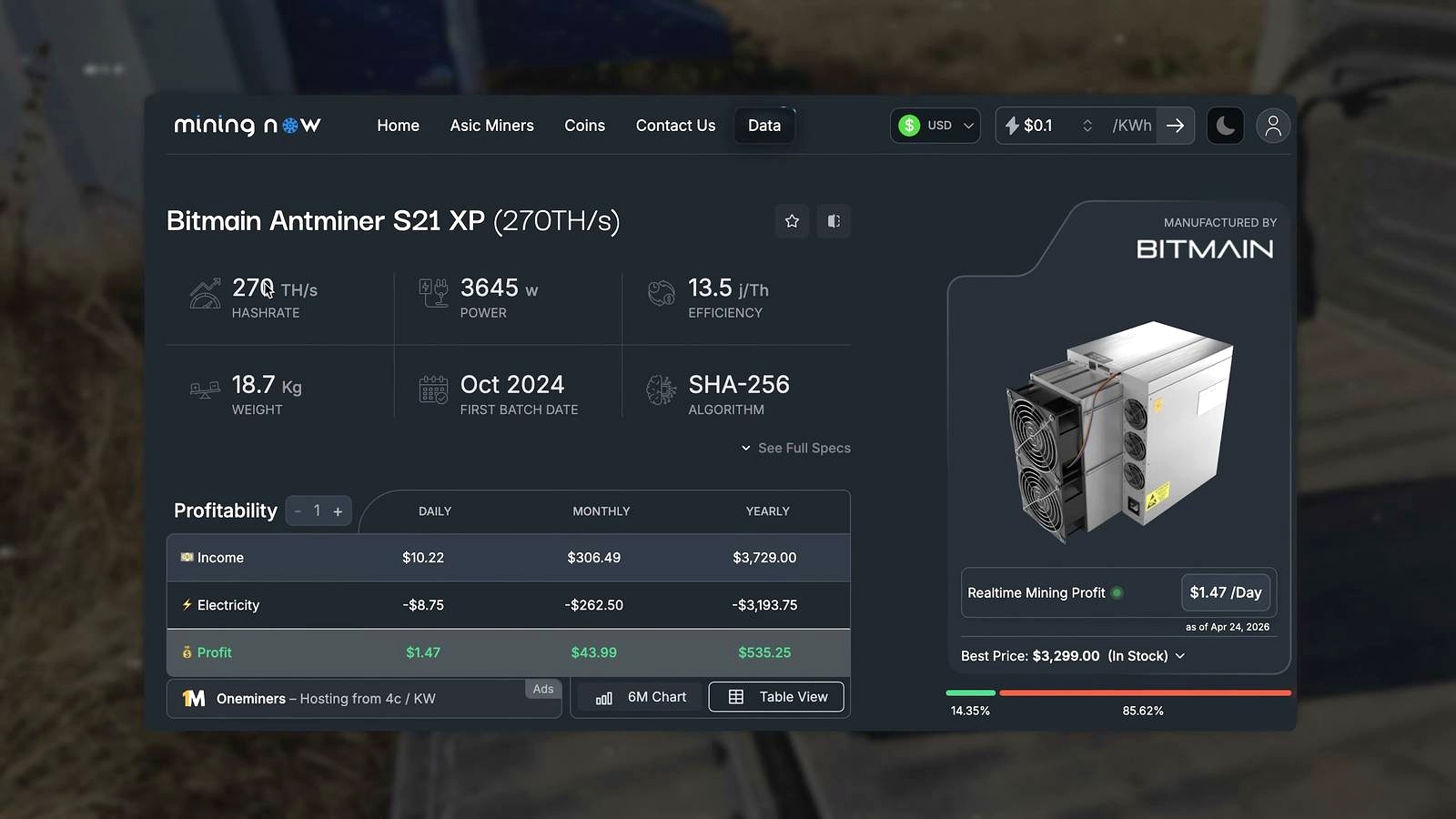

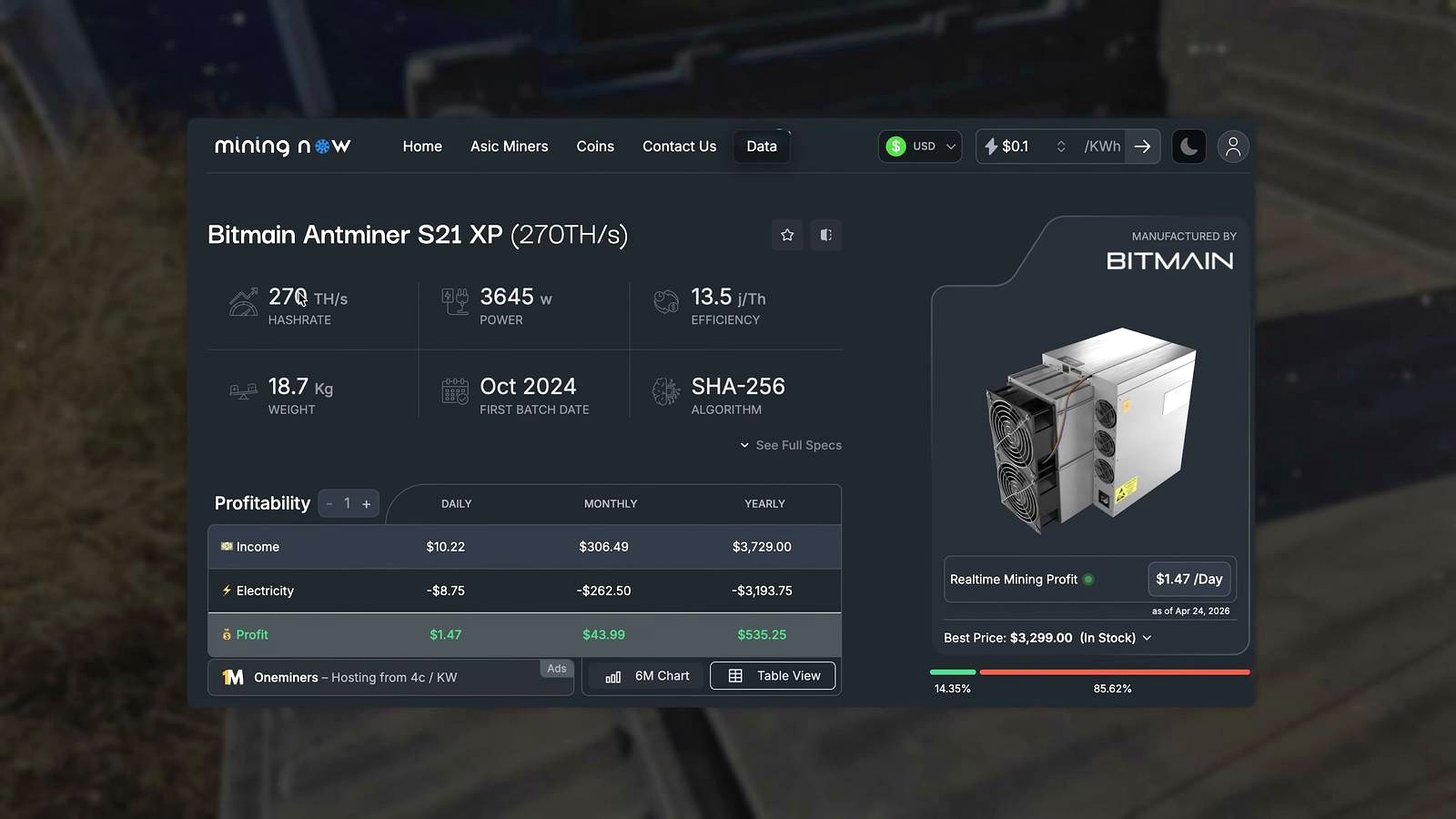

The host uses the Bitmain Antminer S21 XP as his benchmark. He describes it as the best off-the-shelf Bitcoin miner available right now, with a hashrate of 270 terahashes per second and power draw of 3,645 watts. At his cited assumptions, the machine would mine about $10.33 in bitcoin per day. But at an electricity cost of $0.10 per kilowatt hour, he says that operator would spend nearly $9 per day on power and keep just $1.58 daily. For a machine costing well over $3,000, he projects roughly $580 in net annual return after spending $3,200 on electricity. Gross annual bitcoin production, in his framing, is nearly $4,000.

That is a sharp reminder of the post-halving mining reality. Public miners may still scale through financing, fleet upgrades, and access to low-cost energy, but retail miners face a much narrower path. Broader market context supports that caution: mining difficulty has trended structurally higher over time, hashprice remains highly sensitive to fee spikes that rarely persist, and hardware reprices quickly when bitcoin rallies. In other words, a BTC bull market can improve miner revenue while simultaneously making machines more expensive and competition tougher.

VoskCoin also points to Bitcoin issuing $32 million in emissions over the last 24 hours and calls it a $1.5 trillion asset, underscoring the scale of the network. But the editorial takeaway is less about Bitcoin’s size than about who can profitably access that network. In this cycle, scale and cheap power matter more than ever.

Why the Aza Mining Critique Matters

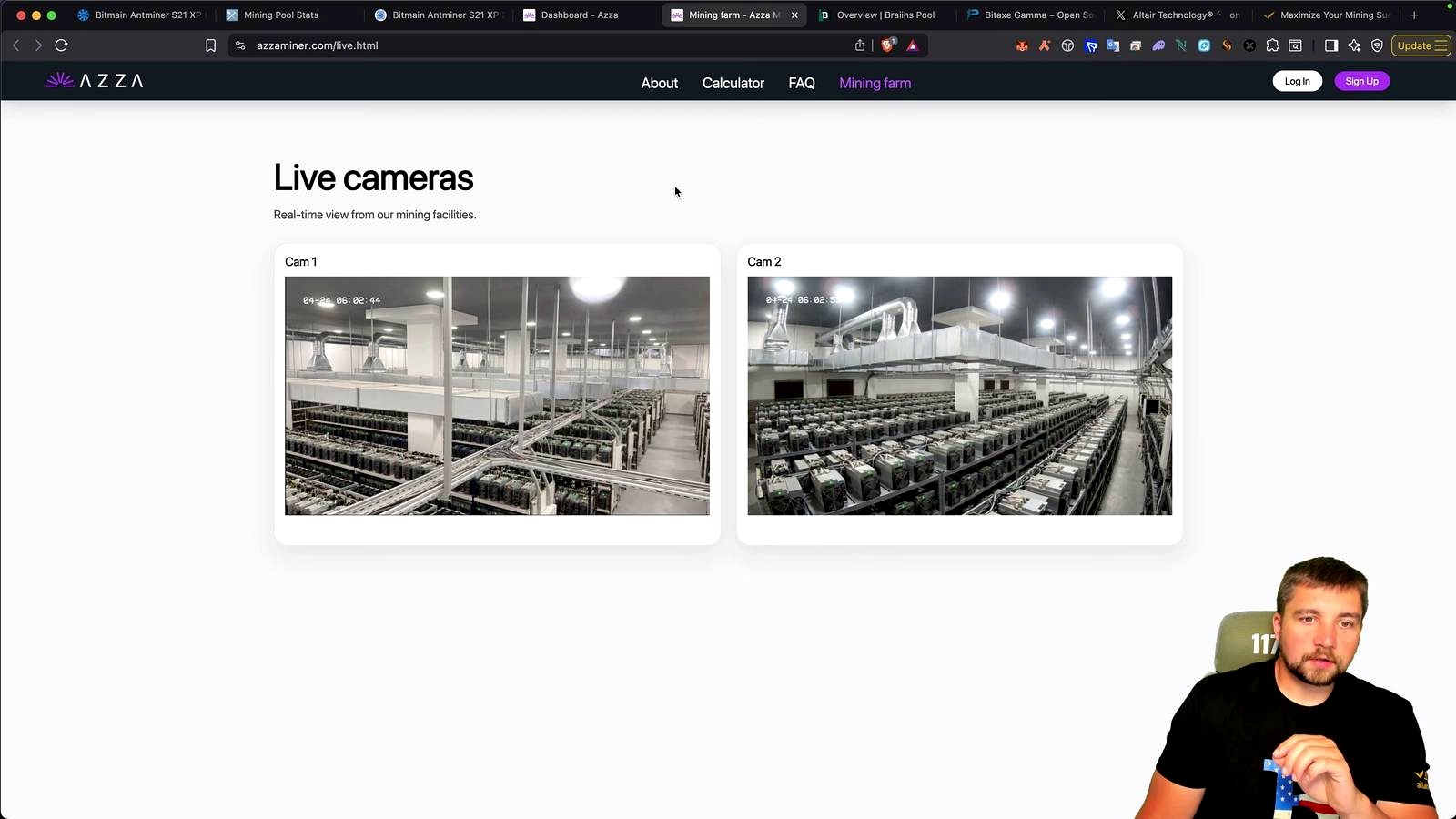

According to VoskCoin, Aza Mining’s attempt to establish credibility may have backfired. The host says the company has business incorporation documents and claims to operate a self-owned, solar-powered Bitcoin mining farm. He also says Aza promoted a livestream of its facility as proof of legitimacy.

His conclusion is blunt: the livestream “looks AI-generated” and “doesn’t look real.” He argues the depicted mining-farm layout makes little physical sense, saying miners appeared to be venting directly into units behind them. He also questions the proportions of the hardware shown and asks where the power cables and front ethernet connections are. Later, he goes further, calling the footage fake and “really alarming.”

That matters because cloud-mining and hash-rate rental schemes have long thrived in periods when retail investors want Bitcoin exposure but cannot justify buying physical ASICs. The less profitable direct mining becomes, the easier it is for turnkey offers to market convenience as a solution. VoskCoin says Aza credited deposits quickly and that withdrawals had worked in testing, but he questions the sustainability of the model and highlights how steady platform returns appeared compared with the real-world variability miners usually experience from outages, hashrate fluctuations, and hosting issues.

He says he had previously allocated 1,000 and 3,000 to test the platform. He contrasts that with a lower-risk learning route for beginners, pointing to the Bitaxe Gamma at nearly $100. For larger ASICs, he notes newer equipment is expensive across the board, citing an S23 price of $7,599 and suggesting the performance improvement over the S21 XP may not justify the cost.

VoskCoin’s skepticism hardens after an interview clip in which an Aza representative says the CEO is “Mike, ” says he has been in crypto for over 10 years, and says the Aza project started in 2023. When challenged on whether the model resembles a Ponzi because users cannot withdraw the initial principal while being shown guaranteed returns, the representative denies it and says the firm already has the equipment and energy. For the host, that was not enough. He says “don’t trust, verify, ” and ends by saying he cannot recommend Aza Mining.

What Could Go Wrong

The obvious pushback is that VoskCoin may be right about retail mining economics but still wrong about a specific operator. A poor-quality livestream, awkward marketing, or incomplete public disclosures do not by themselves prove fraud. A legitimate company can communicate badly, especially in an industry where many operators are private and site access is restricted for security reasons.

There is also a market-based challenge to his hardware pessimism. If Bitcoin keeps rallying sharply, transaction fees rise, or hashprice improves faster than difficulty, payback periods on ASICs can shorten meaningfully. His profitability math is highly sensitive to BTC price, network difficulty, uptime, and electricity cost. At power rates far below $0.10 per kilowatt hour, the economics look different.

Still, the stronger counterpoint to the counterpoint is structural: even in bull markets, cloud-mining buyers usually face layered risk. They depend on a company’s solvency, actual access to machines, truthful reporting, and contract terms they often do not control. The transcript also surfaces one risk not fully developed by the host: counterparty opacity. If key personnel are not clearly listed on a website and operating assets are difficult to independently verify, users are effectively underwriting a private business with limited transparency.

The thesis breaks if Aza provides hard, verifiable proof of owned infrastructure, real-time operating data, public team identities, and a coherent explanation for the discrepancies in its promotional material. Without that, skepticism remains the rational default.

What to Watch Next

For mining economics, watch whether ASIC prices continue rising faster than BTC miner revenue. If hardware inflation outpaces gains in hashprice, retail returns will stay compressed. Monitor power-cost assumptions around $0.10 per kilowatt hour, since that is where VoskCoin’s example becomes barely profitable.

For Aza specifically, the next real catalyst is verification, not marketing. Investors should look for independently confirmable facility footage, public corporate officers beyond a Telegram presence, miner fleet details, and evidence that payouts map to real operating variability rather than unnaturally smooth returns. If those data do not appear, the thesis shifts from caution to avoidance.

FAQ

What is hashprice in Bitcoin mining?

Hashprice is a mining industry metric that estimates how much revenue a miner earns per unit of hashrate, usually per terahash per day. It changes with Bitcoin’s price, transaction fees, block subsidy, and total network difficulty.

Why does electricity cost matter so much for ASIC miners?

ASICs run continuously and consume large amounts of power. In VoskCoin’s example, a machine drawing 3,645 watts earns about $10.33 daily in bitcoin but burns nearly $9 a day in electricity at $0.10 per kilowatt hour. That leaves very little margin.

How is cloud mining different from owning a physical miner?

With a physical miner, you own the machine and can usually verify its operation directly, even if hosting is outsourced. With cloud mining, you are typically buying a contract or exposure to rented hashrate, which adds counterparty risk and often leaves you with limited visibility into the actual hardware.

What is an ASIC miner?

An ASIC, or application-specific integrated circuit, is a machine built for one task: mining a specific cryptocurrency algorithm. For Bitcoin, ASICs are optimized for SHA-256 and are far more efficient than general-purpose computers.

Why can mining returns look “too smooth” on some platforms?

Real mining output usually fluctuates because of pool luck, network difficulty changes, downtime, internet outages, firmware issues, and hosting interruptions. If a platform shows unusually steady returns, users may question whether those payouts reflect actual mining performance or a synthetic accounting model.

Reference Video

Omar Al-Sharif lives and works in the UAE and is involved in the blockchain technology industry. He writes articles on Bitcoin and digital assets as a personal passion, explaining complex topics in simple and understandable language.