Something is shifting in plain sight. What looks like a simple ETF filing is starting to feel more like a quiet power grab, and that is why this moment has people suddenly paying attention.

The headline is obvious. The deeper story is not. A roughly $10 trillion giant is no longer just standing near the door of crypto — it appears ready to walk through it.

The Bloomberg moment that changed the tone

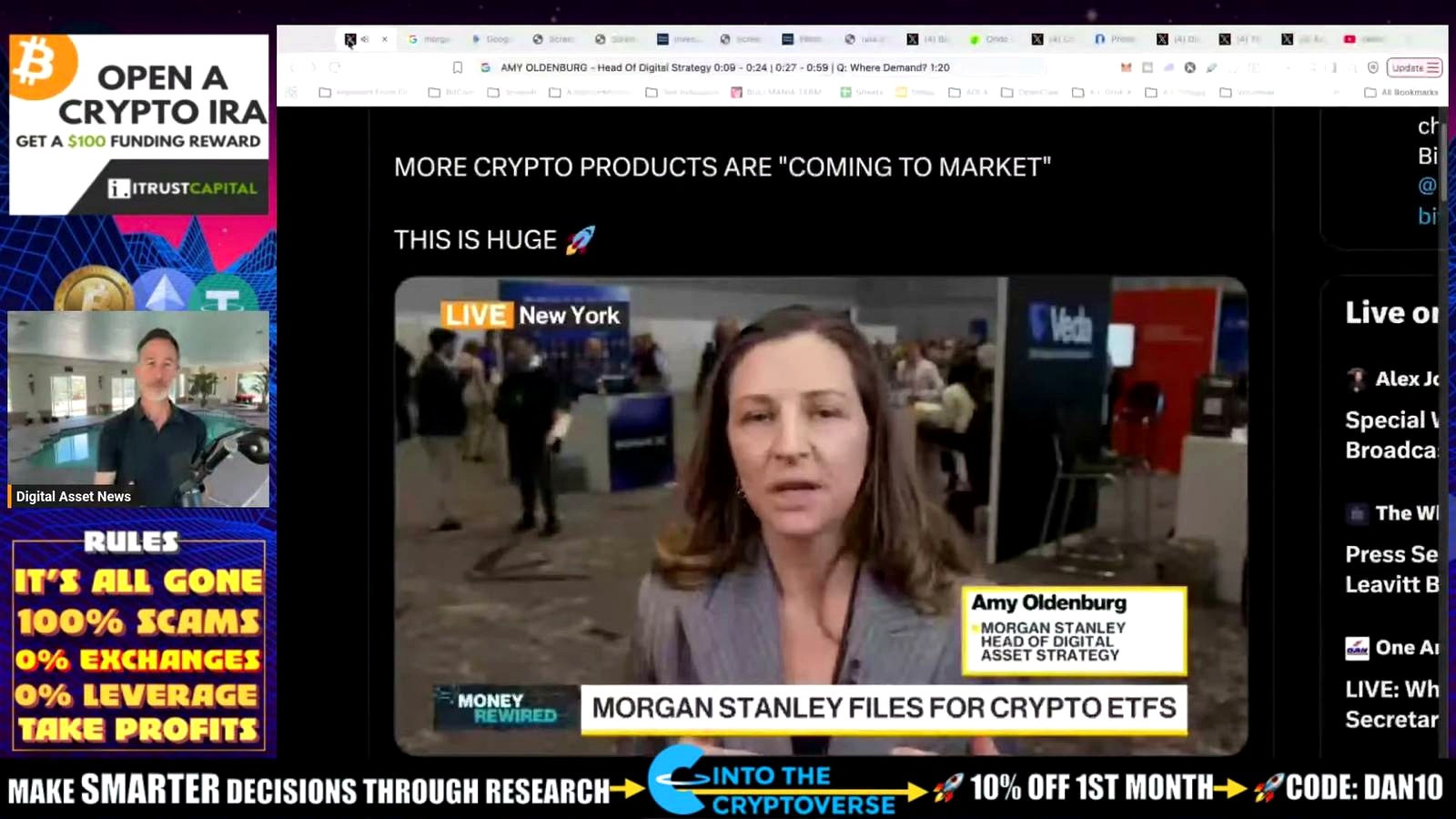

A Bloomberg segment highlighted that Morgan Stanley filed for a Bitcoin ETF under the ticker MSBT. If approved, the firm would become the first major US bank to directly issue and sponsor its own spot Bitcoin ETF.

That alone is a major development. But the real tension sits underneath it: this may not be just another product launch. It may be a signal that a traditional finance heavyweight wants a much bigger role in the Bitcoin economy.

What Morgan Stanley actually said

Amy Oldenberg, head of digital asset strategy, did not say much directly. Her comments were careful and restrained. She said she did not want to talk too much until the product becomes effective, but added that the reasons behind the move would become clearer once it goes live.

She also pointed to something important:

- most activity is still coming through self-directed channels

- there is still more to do on the ETP side

- more products are still needed in the market

On the surface, it sounded standard. In context, it sounded like preparation.

Why this is not just about fees

It would be easy to reduce this to a fight over management fees. That is part of the story, but not the full one.

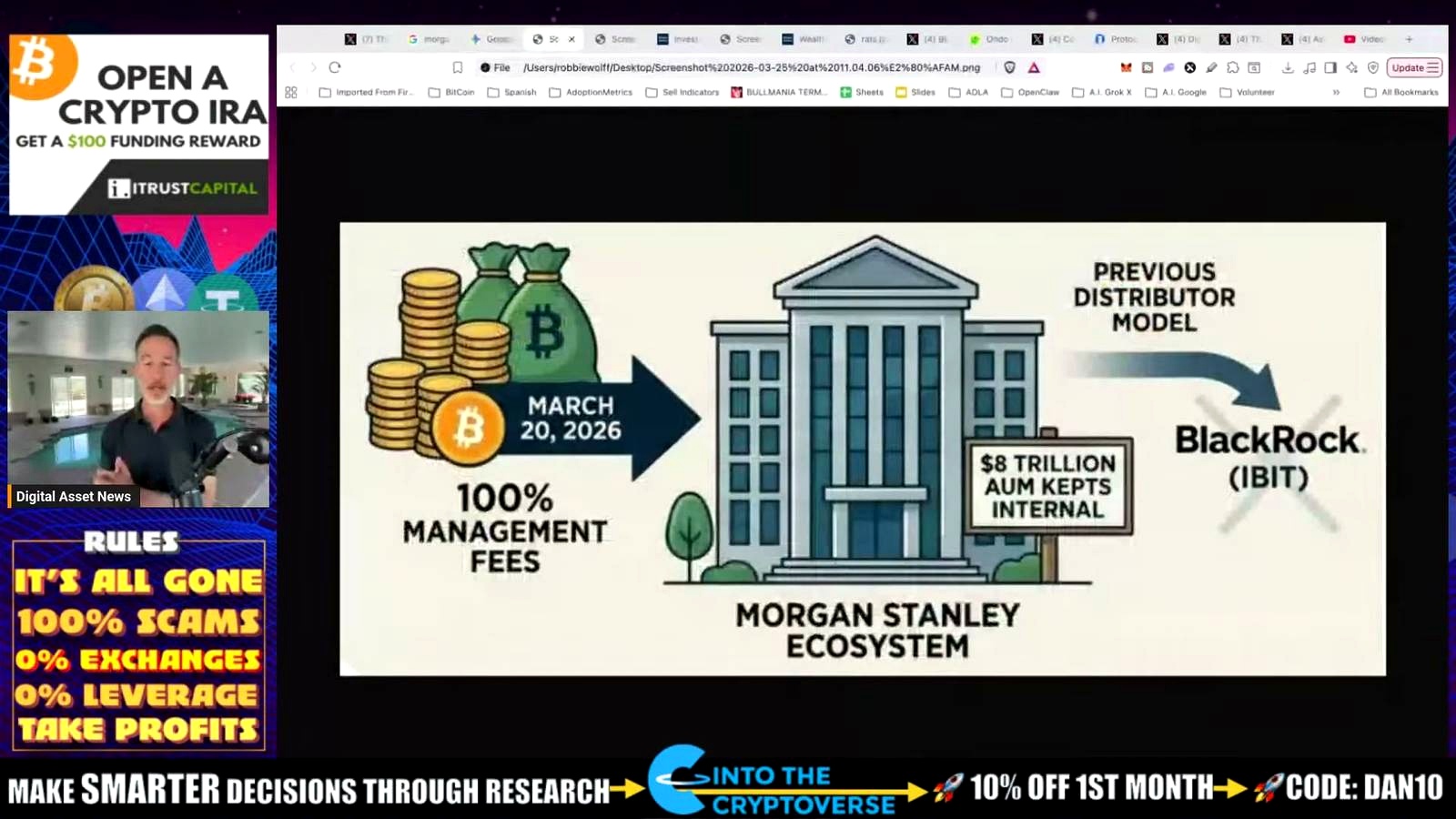

The bigger issue is control.

Morgan Stanley had already been involved as a middleman in bringing BlackRock’s IBIT Bitcoin ETF to market. BlackRock captured the attention and, according to the commentary around the move, made huge gains from it. That experience appears to have changed the equation.

Now the logic looks different: why remain the middleman when you can be the issuer?

The middleman problem

According to the material, Morgan Stanley was caught flat-footed when demand for spot Bitcoin ETFs became impossible to ignore. The assumption had been that demand was limited. Then the market proved otherwise.

That helps explain why this new filing matters. It suggests Morgan Stanley does not want to simply help someone else build the product anymore. It wants to own the product.

- Collect the fees directly

- Control the customer relationship

- Keep more of the upside inside its own platform

That is a very different posture from just helping another asset manager win.

The real target may be Bitcoin wealth itself

Oldenberg’s most revealing point was not just about exposure to Bitcoin. It was about what happens after that exposure enters the traditional finance system.

She said the firm is seeing long-term Bitcoin and crypto holders looking to move some of those assets into traditional finance, where Morgan Stanley can offer other services around that exposure and the wealth created in crypto.

That is where this starts to look like a Trojan horse.

Bringing two worlds together

The SEC allowing in-kind transfers into ETPs was highlighted as a major opening. In practical terms, the material frames this as a way for crypto holders to move assets into ETPs and then be offered additional services.

That creates a new pipeline:

- Bitcoin holders move assets into an ETP structure

- those assets now sit inside a traditional finance environment

- the bank can offer wealth management and related services around that capital

In other words, the ETF may not be the destination. It may be the entry point.

The mandate is already there

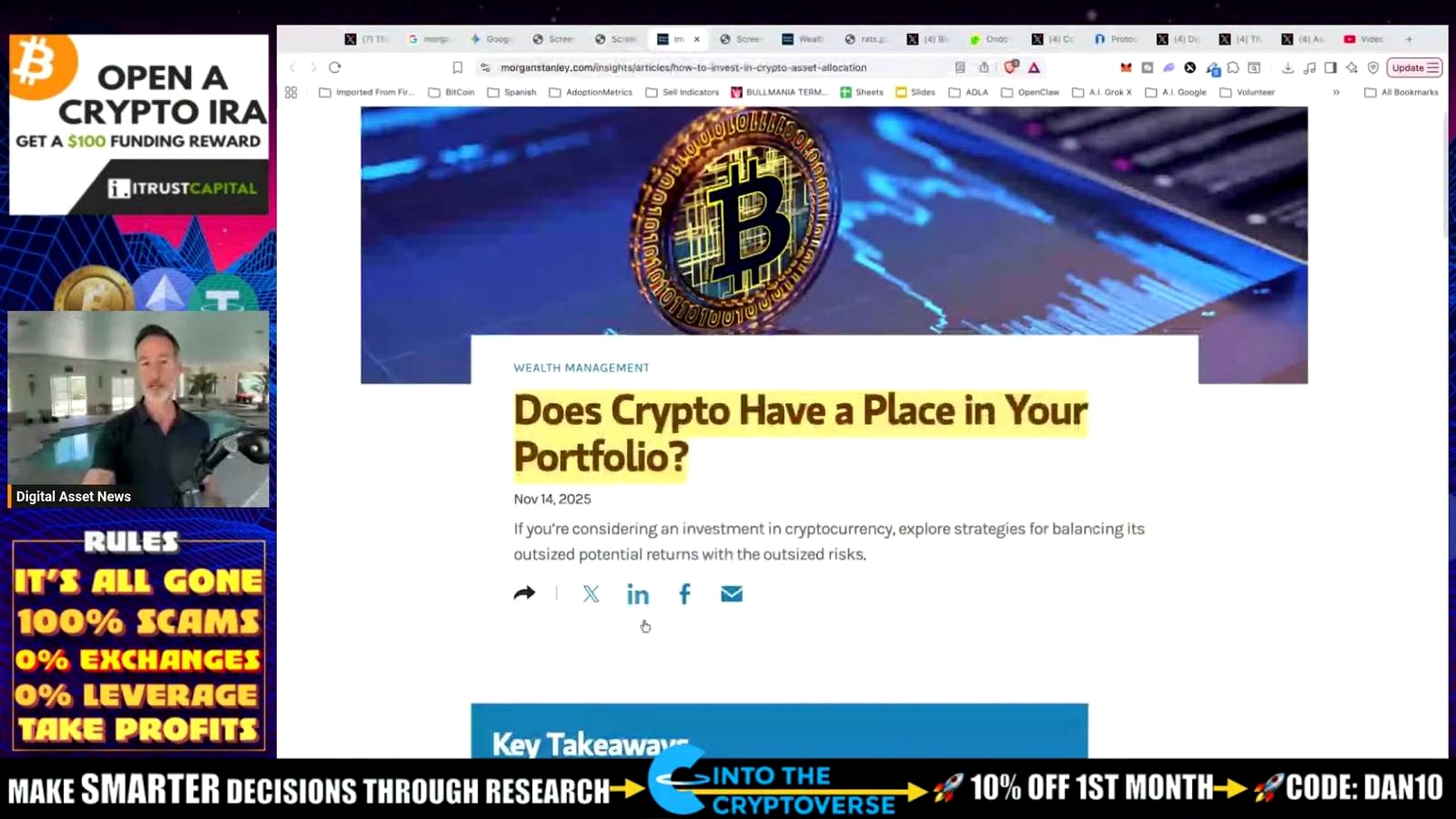

This move also fits with Morgan Stanley’s own published portfolio framing. A November 14, 2025 post on its site asked whether crypto has a place in a portfolio and answered with a clear allocation framework.

The recommendation presented was:

- 2% to 4% crypto exposure in moderate to aggressive growth-oriented portfolios

- 0% in more conservative portfolios

The language was cautious, emphasizing strong return potential but also high volatility and steep potential declines. Still, the important part is simple: a major firm had already carved out a place for crypto exposure.

That changes the mood around this filing. It no longer feels random. It feels aligned with an internal mandate.

Why the allocation math gets attention

The commentary attached to this move pushed the idea further. If a firm with around $10 trillion in assets under management begins to treat Bitcoin exposure more seriously, even small percentages become huge numbers.

The argument laid out was straightforward:

- if just 1% to 2% is allocated, the size is enormous

- the estimate offered was around $160 billion

- that dwarfs the scale referenced for IBIT, which was described as being around $50 billion and later more like $62 billion

The point is not that this has already happened. It is that the math alone makes the filing hard to dismiss.

The old guard is changing its language

One of the more striking themes in the material is cultural, not technical. As wealth in Bitcoin and crypto has grown, traditional institutions that once dismissed the space are now moving closer to it.

That tension came through in a blunt observation: banks want Bitcoin, while many ordinary people still struggle to convince friends it is not a scam.

That gap matters. It suggests the public conversation is lagging behind what institutions are already doing in the background.

From skepticism to product strategy

The material leaned into the irony. The same financial world that once used terms like “scam,” “Ponzi,” or even “rat poison squared” now looks increasingly willing to build products, collect fees, and serve crypto-generated wealth.

That does not mean all skepticism is gone. It means incentives are getting louder.

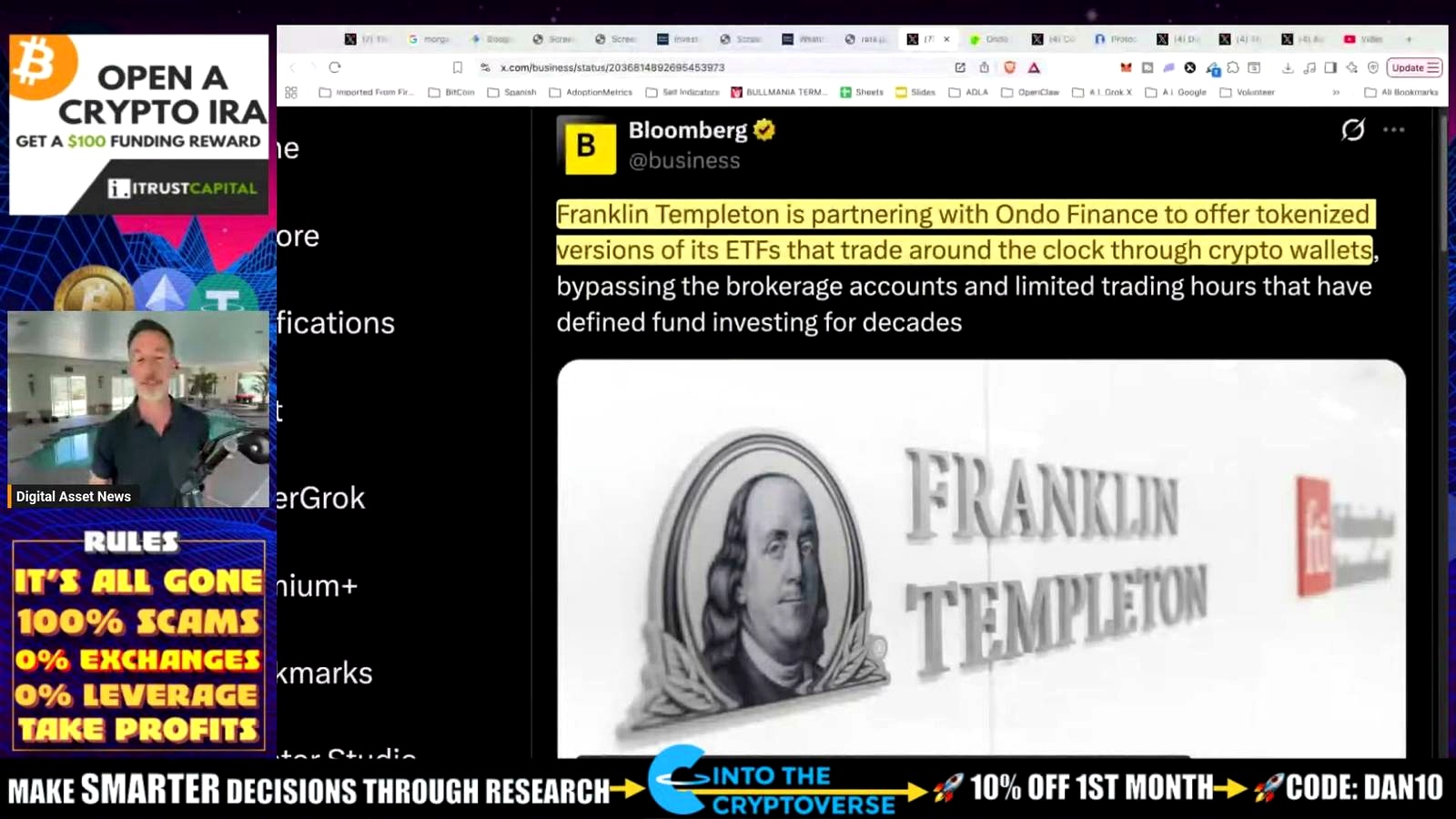

Tokenized assets are heating up too

The Morgan Stanley story did not arrive in isolation. Another institutional development mentioned alongside it was Franklin Templeton partnering with Ono Finance to offer tokenized versions of its ETFs.

The description was simple: tokenized assets seem like the new hot play right now.

There was also caution. The related asset performance discussed in the material was weak over longer periods, including a decline of roughly 72% over the last year, despite a short-term uptick. The message was not blind optimism. It was that stories like this help gauge direction, even if price action remains messy.

Why these stories matter together

Put side by side, they suggest a broader pattern:

- traditional finance is moving deeper into Bitcoin products

- tokenized ETF structures are being explored

- the wall between crypto and traditional finance is getting thinner

That does not guarantee outcomes. But it does make the moment feel active, not theoretical.

What institutions seem to want — and what they ignore

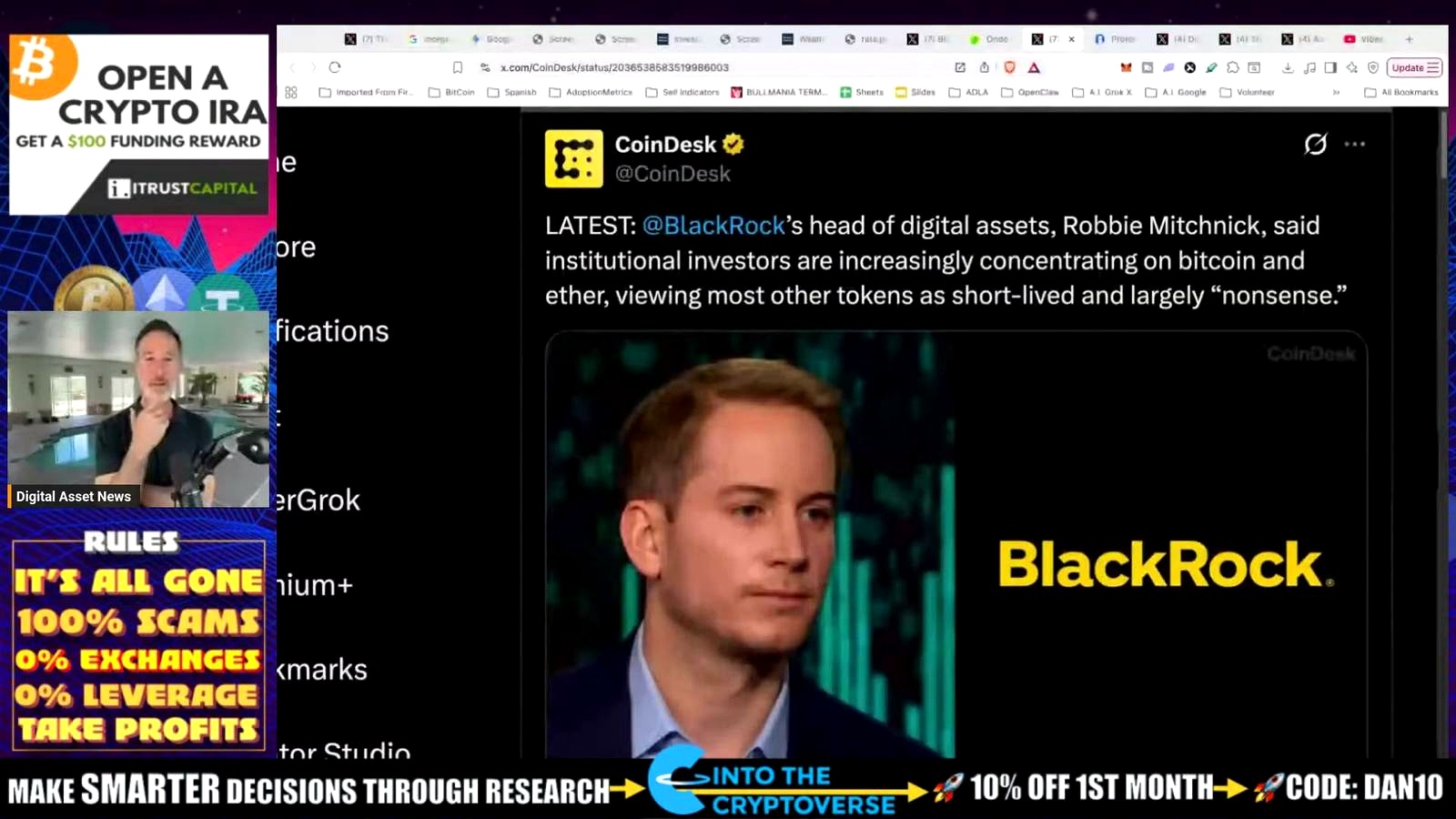

BlackRock digital assets head Robbie Mitchnik was cited as saying institutional investors are increasingly concentrating on Bitcoin and Ethereum, while viewing many other tokens as short-lived or largely nonsensical.

That is one institutional view. The material pushed back by pointing to what cannot be easily faked: fees and actual usage.

The on-chain fee argument

Using DeFi Llama fee data discussed in the material, the case was made that real adoption shows up in revenue and network activity, not just in Wall Street narratives.

Figures cited included:

- $46 million in fees over 24 hours

- historical growth from roughly $10 million to $20 million per day to peaks of $240 million on January 20, 2025

- another period in October reaching over $100 million and nearly $200 million per day

The biggest fee drivers mentioned were Tether and Circle, with Ethereum, Binance, Solana, and Tron identified as top chains connected to them.

Other names highlighted included:

- Hyperliquid

- pump.fun

- Lido

- Uniswap

Ethereum was described as accounting for about $8 million out of the $46 million in daily fees referenced, with Solana at about $5 million, Hyperliquid at about $2.49 million, and Base at about $1.46 million.

The broader argument was clear: institutions may focus on Bitcoin and Ethereum, but the wider market is showing signs of life through usage and fee generation.

The bullish case comes with a warning

For all the excitement, the material did not end in celebration. It ended with a reality check.

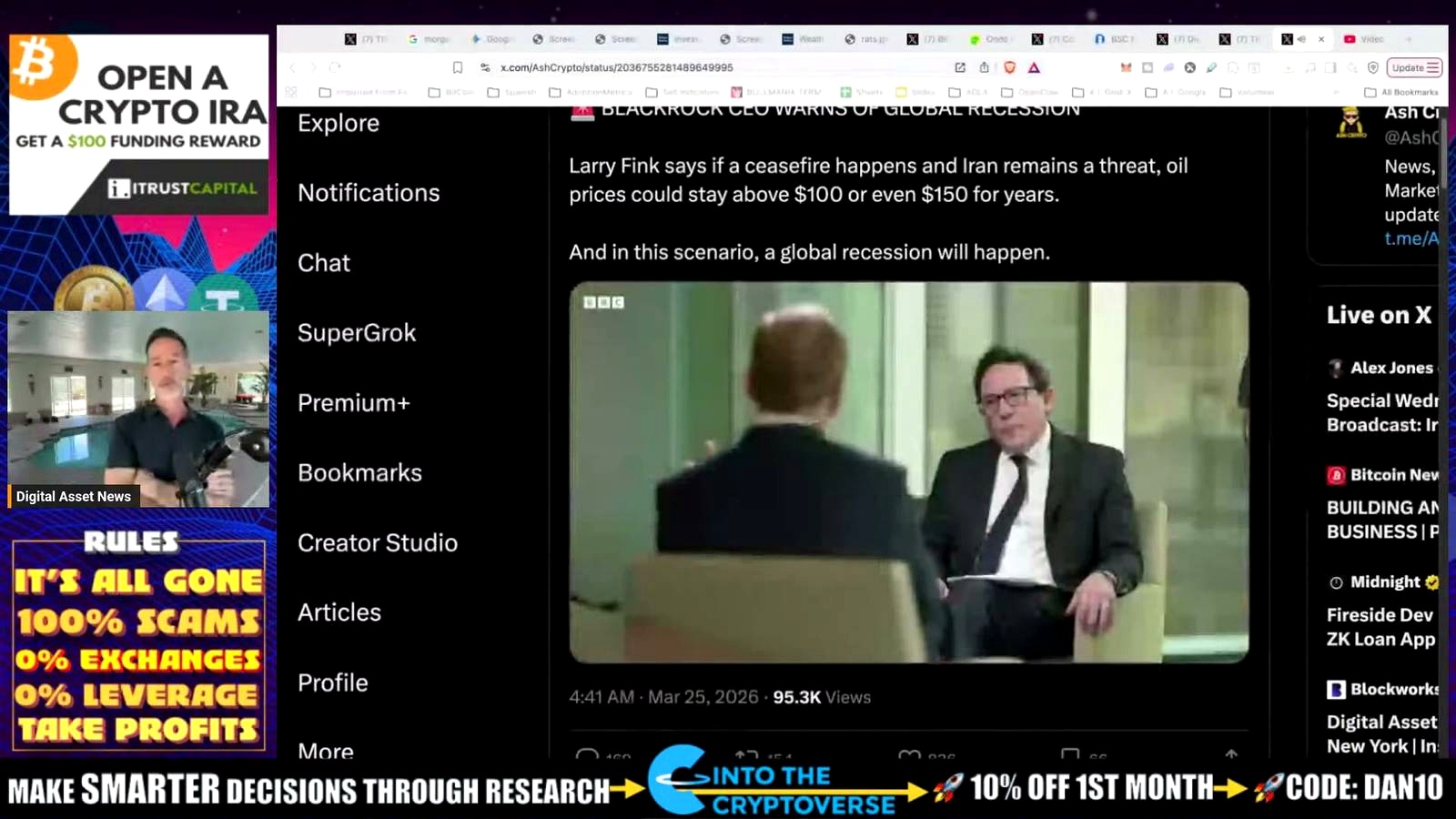

Larry Fink warned that if a cessation of war happens but Iran remains a threat to trade and the Strait of Hormuz, oil could stay above $100 and closer to $150. His conclusion was blunt: that would mean a global recession.

That warning changes the mood around everything else.

Why this still matters

Even if Morgan Stanley’s Bitcoin plan is as significant as it looks, it does not exist in a vacuum. Institutional momentum can build at the same time that macro risks get worse.

That is what makes this moment feel so charged. There is clear movement inside traditional finance. There is visible appetite to pull crypto wealth into bank-managed channels. There are signs of product expansion and deeper integration.

And yet the broader backdrop still has the power to hit everything at once.

FAQ

What did Morgan Stanley file for?

Morgan Stanley filed for a Bitcoin ETF under the ticker MSBT, which would make it the first major US bank to directly issue and sponsor its own spot Bitcoin ETF if approved.

Why is this Morgan Stanley Bitcoin ETF filing seen as such a big deal?

Because the move appears to be about more than launching another ETF. It points to direct control over fees, product ownership, and access to crypto-generated wealth inside Morgan Stanley’s traditional finance platform.

What did Amy Oldenberg say about the plan?

She said she did not want to say too much before the product becomes effective, but suggested the reasons for the move would become clearer when it goes live. She also said more products still need to come to market.

How could in-kind transfers change the game?

The material suggests SEC approval for in-kind transfers into ETPs could allow Bitcoin and crypto holders to move assets into these products more directly, opening the door for banks to offer additional financial services around that wealth.

What is Morgan Stanley’s current view on crypto in portfolios?

The firm’s cited framework suggests 2% to 4% crypto exposure for moderate to aggressive growth-oriented portfolios and 0% for more conservative portfolios, while acknowledging high volatility and steep potential declines.

Why are people calling this a “Trojan horse”?

Because the ETF may be less about simple exposure and more about drawing Bitcoin wealth into Morgan Stanley’s ecosystem, where the firm can offer broader wealth management and financial services.

What other institutional trends were mentioned alongside this?

Franklin Templeton’s partnership with Ono Finance to offer tokenized ETF versions was highlighted, reinforcing the idea that tokenized assets and crypto-linked financial products are becoming a bigger focus.

What is the main risk hanging over all of this?

The biggest warning raised was macroeconomic: if tensions around Iran threaten trade and push oil toward $150, the result could be a global recession.

Original Source

Omar Al-Sharif lives and works in the UAE and is involved in the blockchain technology industry. He writes articles on Bitcoin and digital assets as a personal passion, explaining complex topics in simple and understandable language.